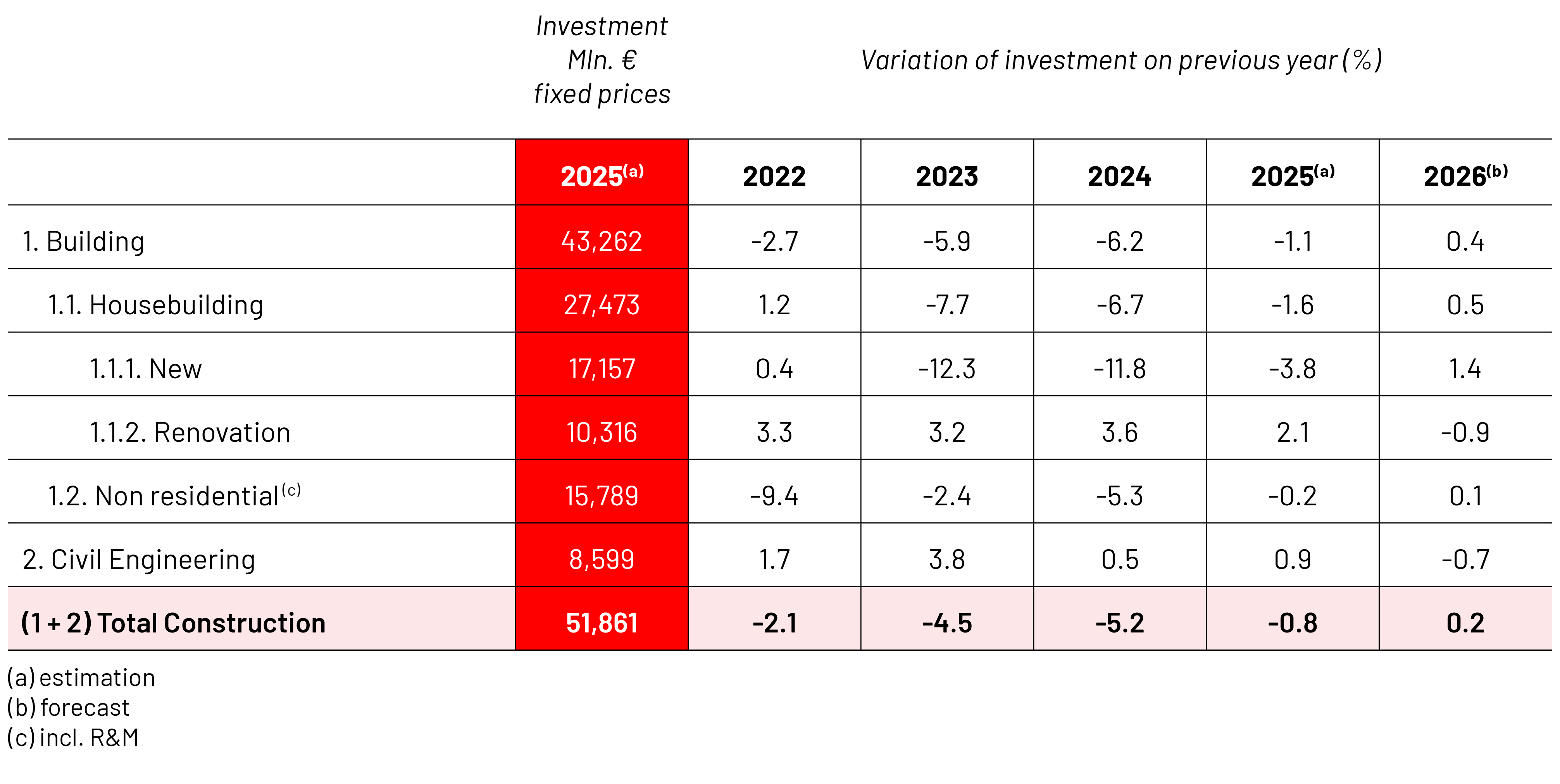

Overall construction activity

After two years of recession, Austria was entering a fragile recovery after declines of 0.8% (2023) and 0.7% (2024). The current war in the Persian Gulf, however, has strongly negative effects on the overall economic development. Therefore, WIFO has reduced the GDP forecast for 2026 to 0.9%. Employment stagnates and unemployment peaks at 7.5% in 2025 before edging down to 7.3% in 2026.

Situation in construction is diverse: residential building improves earlier than equipment investment thanks to falling interest rates, while public austerity drags on civil engineering (ÖBB plan trimmed, Vienna metro delays, Styria road cuts).

Housebuilding

Austria’s housing cycle was stabilizing in 2025: WIFO expects residential construction at +0.5% in 2026. New-build is 2026 expected with a modest upturn (+1.4%), while renovation – previously buoyed by high energy prices and generous subsidies – slows as fiscal consolidation bites. Building permits remain far below the 2019 peak but turned up in 2025H1 (+12.8% y-o-y change nationally).

Non-residential construction

The sector has been heavily affected by the recession of 2023–2025, with private investment-driven segments such as industrial, office, and commercial buildings experiencing sharp declines. Persistently weak economic growth, high financing costs, and fiscal consolidation measures have suppressed both private and public investment in construction. Publicly financed construction, particularly in education and healthcare, faces spending cuts and prioritization due to budgetary pressures, though selective increases in funding for essential and sustainable projects continue. Industrial building activity remains constrained by weak exports, while office and commercial construction are weighed down by subdued domestic demand despite early signs of improvement in financing and sentiment. Gradual stabilization is projected for 2026, with stagnation in non-residential output overall, before a moderate recovery from 2027 onward driven by improved macroeconomic framework.

GDP 2025

BILLION

POPULATION 2025

Total investment in construction in 2025

BILLION

Civil engineering

Civil engineering remained resilient until 2024, stimulated primarily by transport and energy infrastructure investments. However, the fiscal constraints introduced in the 2025/26 federal budget are now dampening investment growth, which is projected to stagnate in 2026, and decline thereafter. Road, rail, and water infrastructure will be most affected by budget consolidation, with significant declines forecasted toward 2028. While ASFINAG’s highway expansions and ongoing railway tunnel projects continue, reduced provincial and municipal funding will delay or scale down numerous initiatives. Telecommunications investment, after rapid 5G rollout, will decline due to lower public subsidies and market saturation, whereas the energy sector’s momentum is dampened by new taxes and moderating profits despite EU support. Water management faces the steepest challenges as tighter funding and stricter requirements weigh heavily on smaller municipalities, further exacerbating the expected drop in public investment through 2028.

Prices of construction materials

Due to war in Persian Gulf, oil market is currently extremely critical. In addition to the rising oil prices and the massive cost impacts on many derivatives and subsequent products, key transport routes in the region are restricted and affect the supply situation on numerous key building products. The cumulative uncertainties of cost developments force construction companies to take risks that cannot be calculated.

Business registration and bankruptcy

The construction industry recorded in 2025 an increase in company registrations of about 5% compared to the previous year. In contrast, the number of bankruptcy filings decreased slightly by 0.7% compared to 2024.

Construction Activities

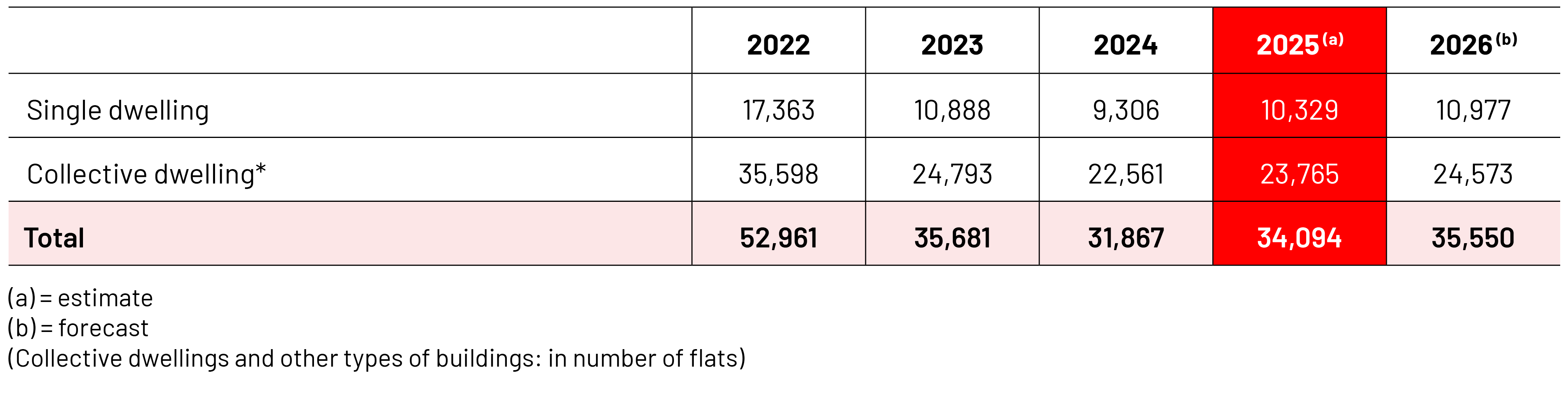

Number of building permits in residential construction