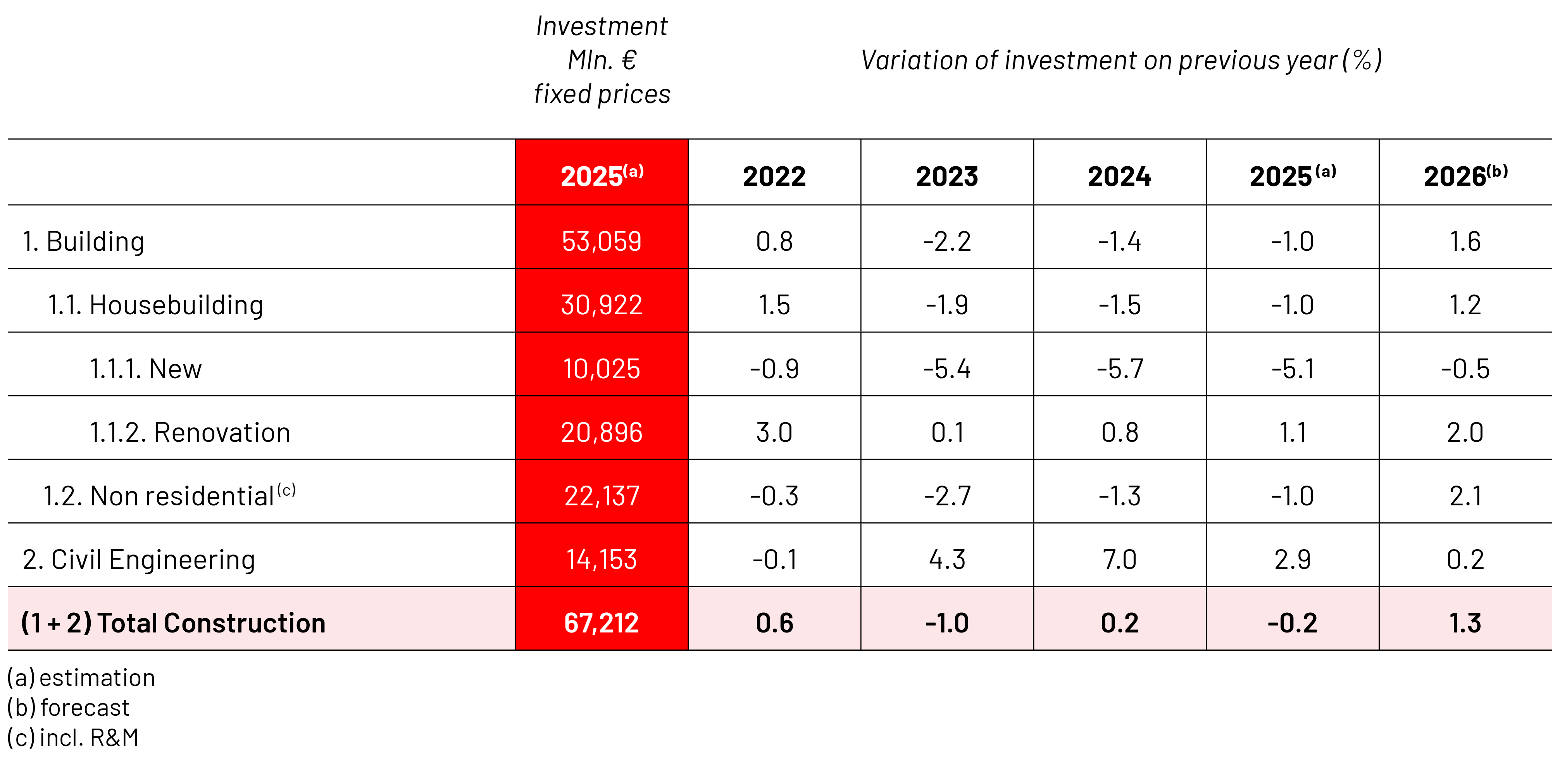

Overall construction activity

Overall, the construction sector likely experienced a slight decline in 2025 (-0.3%). This occurred in a context still marked by difficulties related to cost levels and interest rates, both of which continued to strongly affect the residential sector.

Concerning 2026, the Gulf crisis has created a global economic environment less favorable than in 2025 and has generated new increases in material prices, clearly affecting the construction sector. Nevertheless, the outlook for new housing is less negative than the trends observed in recent years. Although still decreasing on an annual average basis, building permits did show growth during the second half of 2025.

Thus, unlike previous years, it appears that no subsector should experience a sharp decline in 2026. And unlike previous years, the growth of certain subsectors will not be cancelled out by declines in others.

Under these conditions, construction as a whole could grow by around 1.3% in 2026.

Residential construction

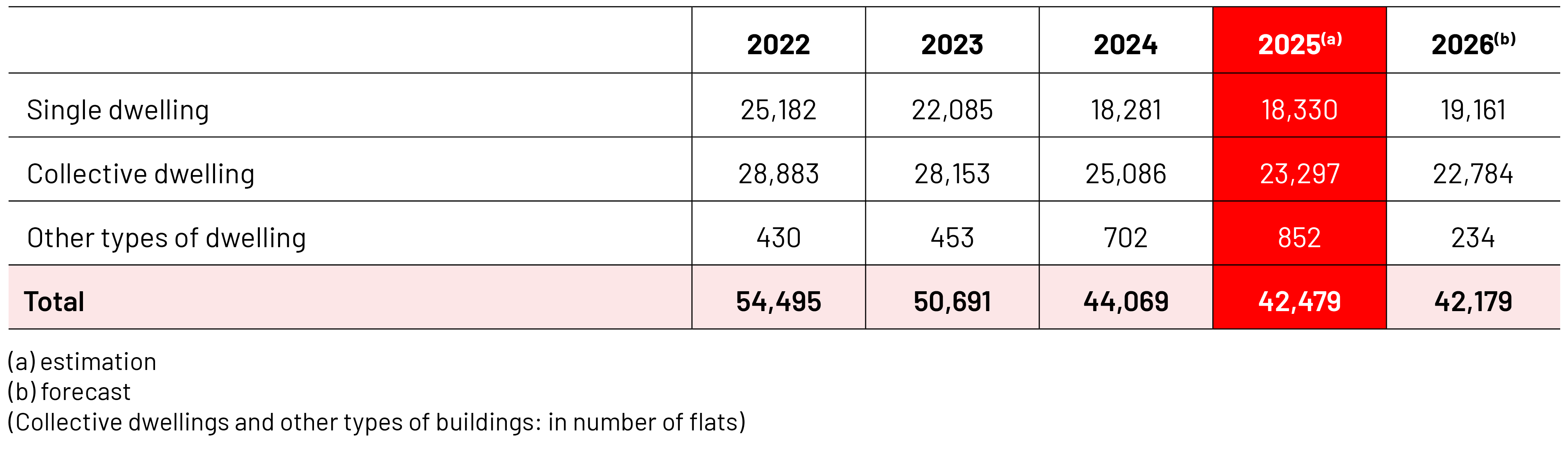

Activity related to the construction of new housing experienced another significant decline in 2025 (-5%), given the sharp drop in the number of authorized dwellings, which continues to fall on an annual average basis. However, the second half of the year showed a reversal of this trend. This reversal is expected to be short‑lived. Geopolitical developments in early 2026 in the Persian Gulf region have changed the situation, leading in particular to rising unemployment and a decrease in disposable income. As a result, there is concern that the number of newly authorized dwellings will quickly resume its downward trend.

Nevertheless, it is hoped that the construction of new housing will experience only a limited decline in 2026 (-0.5%). The expected inverted V‑shaped monthly profile of building permits for the 2025–2026 period results in a near‑stabilization of the volume of housing to be built in each of these two years.

Activity in the housing renovation sector continued to grow in 2025 (+1.1%). A final surge in recovery plans and work related to the recent mandatory energy renovation requirement in Flanders more than compensated for the persistent difficulties linked to construction costs and interest rates. Housing renovation is expected to continue growing in 2026 and even accelerate, as the difficulties linked to construction costs and interest rates weigh less heavily on residential projects (judging by the expected trend for new housing).

Non-residential construction

Non‑residential renovation, supported by its own momentum and the ramp‑up of recovery plans, grew by 1.6% in 2025. In 2026, it is expected to grow by another 1.3% despite the gradual completion of recovery plans.

New non‑residential buildings appear to be on track for growth of around 3% in 2026, due in particular to the acceleration of certain major projects and the expected growth in hospital and agricultural buildings. The latter are benefiting from a resumption of investments after a waiting period following the clarification of nitrogen‑related obligations in the sector.

GDP 2025

BILLION

POPULATION 2025

Total investment in construction in 2025

BILLION

Civil engineering

Civil engineering is estimated to have grown by nearly 3% in 2025, thanks to the combination of two favorable factors: the effects of recovery plans and increased investments linked to certain major projects. Conversely, it suffered from a decline in investments by local authorities, as the investment efforts made in anticipation of the 2024 municipal elections had passed.

The total volume of work related to major specific infrastructure projects is expected to remain fairly stable in 2026. Investments in rail infrastructure are expected to increase significantly. Conversely, investments by local authorities are expected to decline further, and recovery plans are not expected to generate as much work as in 2025. Civil engineering activity should therefore remain stable in 2026 (+0.2%).

Prices of construction materials

After the sharp increases of previous years, material prices experienced a period of relative stability from 2023 to 2025. The geopolitical tensions that emerged in early 2026 in the Persian Gulf region, along with the subsequent rise in energy prices, quickly led to new increases in material prices, which in some cases were very significant.

Materials most closely linked to petroleum (fuels, bitumen, plastics) are clearly those for which price increases have been the fastest and most significant.

Futures markets for oil and gas anticipate a gradual normalization of prices, with a decline expected throughout the second half of 2026 and into 2027. This raises hopes that material prices will not surge further and that most of the increase occurred in the months immediately following the emergence of geopolitical tensions in the Gulf. The prospects for lasting peace agreements in the region, which strengthened in June, support this view. However, only time will tell whether this hypothesis holds true, given that the construction materials market does not always evolve rationally and that geopolitics is highly unpredictable.

Number of building permits in residential construction