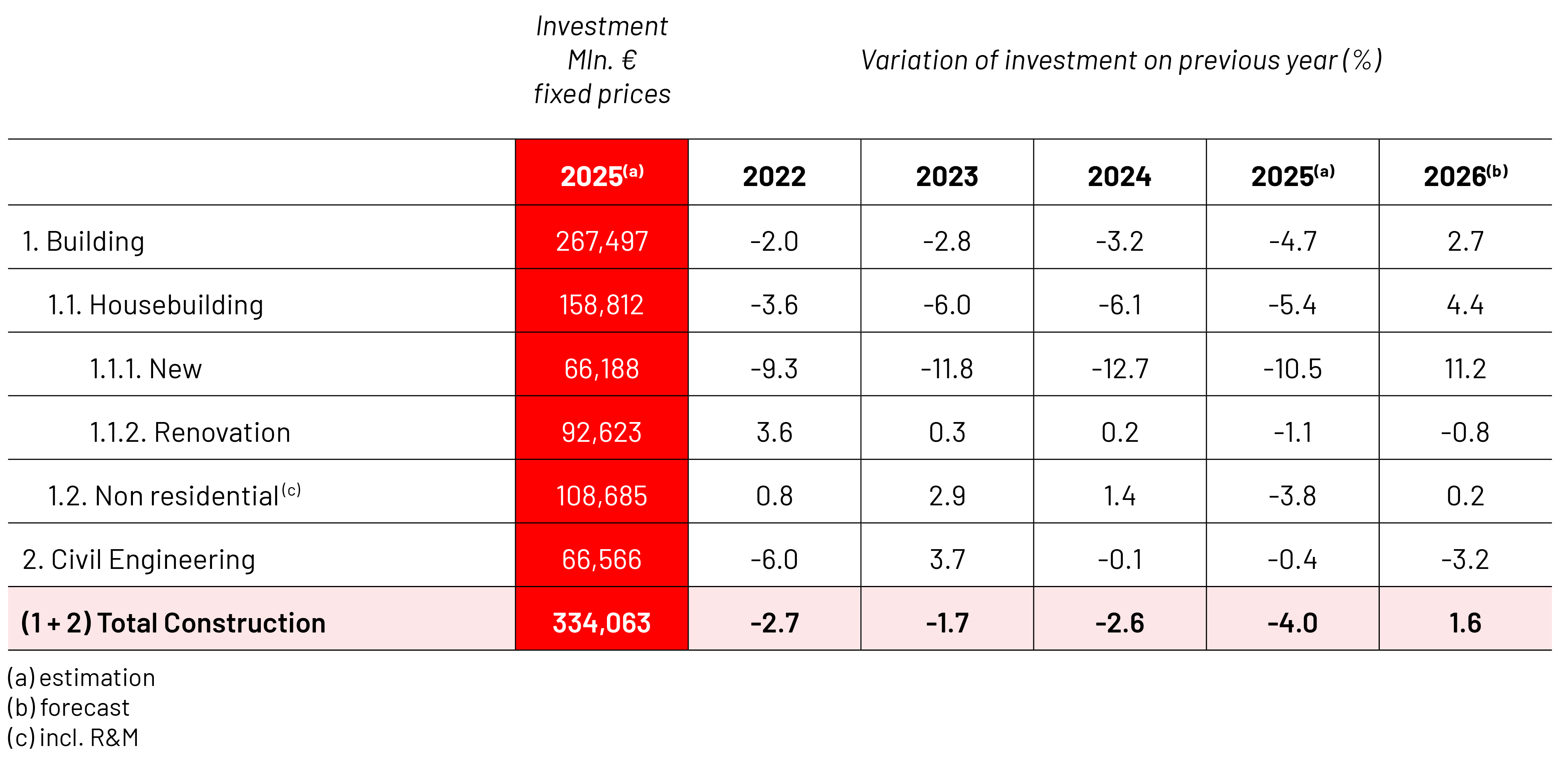

Overall construction activity

In 2025, the construction sector experienced a decline by 4,0% in constant prices in France, mainly due to the negative trend in the building industry (-4,7%), whereas the public works sector remained rather stable (-0,4%).

For 2026, French construction investment is expected to rebound by 1,6% in volume terms, with building returning to growth (+2,7%) while public works should contract (-3,2%).

These variations result in a loss of 19 000 jobs (including employees, temporary workers, and self-employed workers) in 2025 (-0,9%). The expected recovery in construction investment will not be sufficient to reverse this trend, with a further loss of 10 000 jobs in 2026. For public works, 5 000 jobs will be destroyed, following the clear entry into recession.

Housebuilding

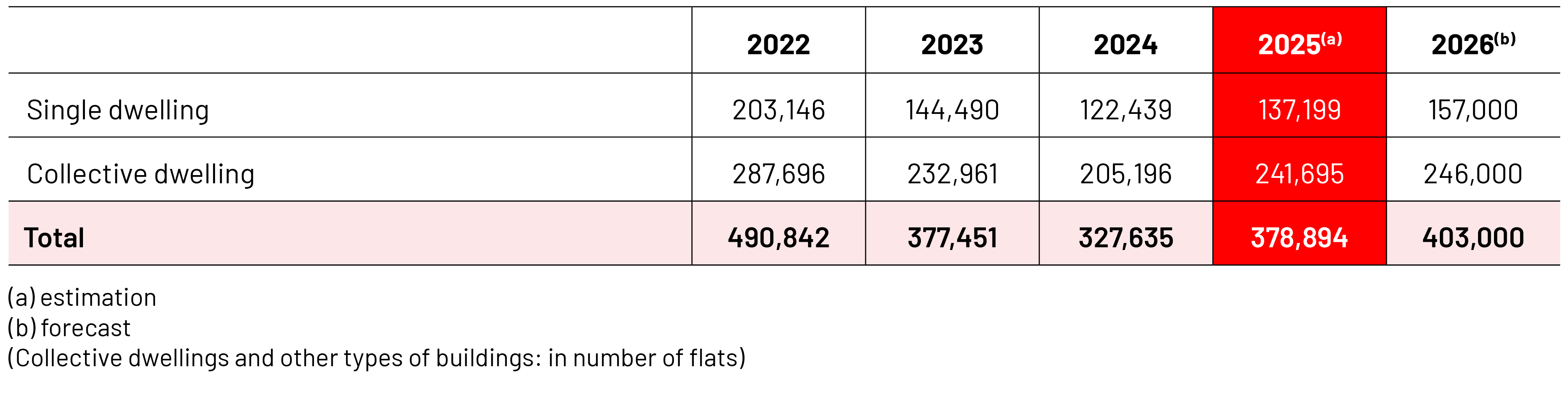

After an increase of 5,3% in 2025, housing starts will continue to grow, by 11,7% in 2026, but at a very low level of 308 000 units (around 50 000 units below the long-term average). New housing permits are expected to improve at a slower pace, by +6,4% on the same period. The individual housing market will maintain its momentum from 2025, carried by the reopening of the zero-interest loan scheme (PTZ) since April 1, 2025. Besides, the collective housing market will also regain some strength, with the implementation of a new tax incentive scheme supporting private rental investment (“Jeanbrun”), and a €400 million cut in the levy on social housing organizations. However, the expected recovery could be weakened by the Middle East conflict, with a likely increase in interest rates and potential delays in household real estate projects.

Given the usual construction timelines and the increase of housing starts in 2025, housebuilding investment will rebound by 11,2% at constant prices in 2026, but it will merely offset the decline by 10,5% in 2025. The market will simply return to the low level of activity of 2024.

The growth in housing rehabilitation and maintenance activity observed since 2021 stopped. Indeed, a 1,1% drop was recorded in 2025, with a further decline by 0,8% expected in 2026. Despite a public budget maintained for energy renovation, this market will continue its retreat, due to the late adoption of the Finance Act. In addition, the volume of non-energy related renovations will contract further, as the majority of transactions do not involve any renovation work.

Non-residential construction

In 2026, construction started surfaces will plateau after a growth by 5,4% in 2025.

Authorized floor spaces will continue to stabilize (-0,2%). More specifically, offices will continue to collapse, but at a slower pace (-7,0%), as supply remains excessive compared to a persistently weak demand. Administrative buildings will turn negative (-8,5%), related to the municipal elections, and hotels will decrease slightly (-2,5%), while other markets – such as industrial buildings or retail spaces – will remain stable. Only agricultural buildings will grow (+6,5%), supported by public subsidies to farmers installing photovoltaic systems.

Thus, after a 6,5% decline in 2025 at constant prices, non-residential building investment is expected to rise slightly by 0,5% in 2026, driven by the rebound of started surfaces in 2025.

The non-residential rehabilitation and maintenance activity will stabilize by -0,1% in constant prices in 2026, after -1,0% in 2025. In more details, growth in corporate investment is expected to support renovation activity, but will be offset by a decline of local authorities’ investment during a year of municipal elections. A similar trend is expected for energy renovation activity.

GDP 2025

BILLION

POPULATION 2025

Total investment in construction in 2025

BILLION

Civil engineering

Public Works activity remains flat in 2025 (-0,4% in volume) following two years of expansion. Although output typically increases ahead of municipal elections, this usual pattern is being dampened by cuts in local authority funding, the ongoing real estate downturn, and persistent political uncertainty. As a result, 2025 runs counter to the usual electoral cycle effect.

A further decline of 3,2% is projected for 2026. While the private sector may benefit from a gradual recovery in the real estate market, the broader economic environment remains subdued, thereby limiting the development of industrial projects. Energy operators are expected to remain dynamic, while large transport projects follow more varied trajectories. Meanwhile, public investment is set to really decrease significantly, reflecting both the less favourable phase of the municipal cycle and ongoing budgetary pressures.

Regarding overseas activity, French companies’ exports reached €66,7 billion in 2025, accounting for 57% of total civil engineering turnover.

Prices of construction materials

On the whole, prices of materials for construction remained broadly stable in 2025, with little variation across products, except for semi-finished aluminium and copper products, which have increased by nearly 5%.

But with the EU Carbon Border Adjustment Mechanism (CBAM) and, much more, the crisis in the Middle East, construction material prices will increase significantly in 2026.

Business registration and bankruptcy

Business registrations in construction declined by 5,6% in 2025. Meanwhile, bankruptcy declarations decreased by 3,1 %, but stayed at a high level of 14 500 units, equivalent to the 2015-2016 average.

Construction Activity

Number of building permits in residential construction