Overall construction activity

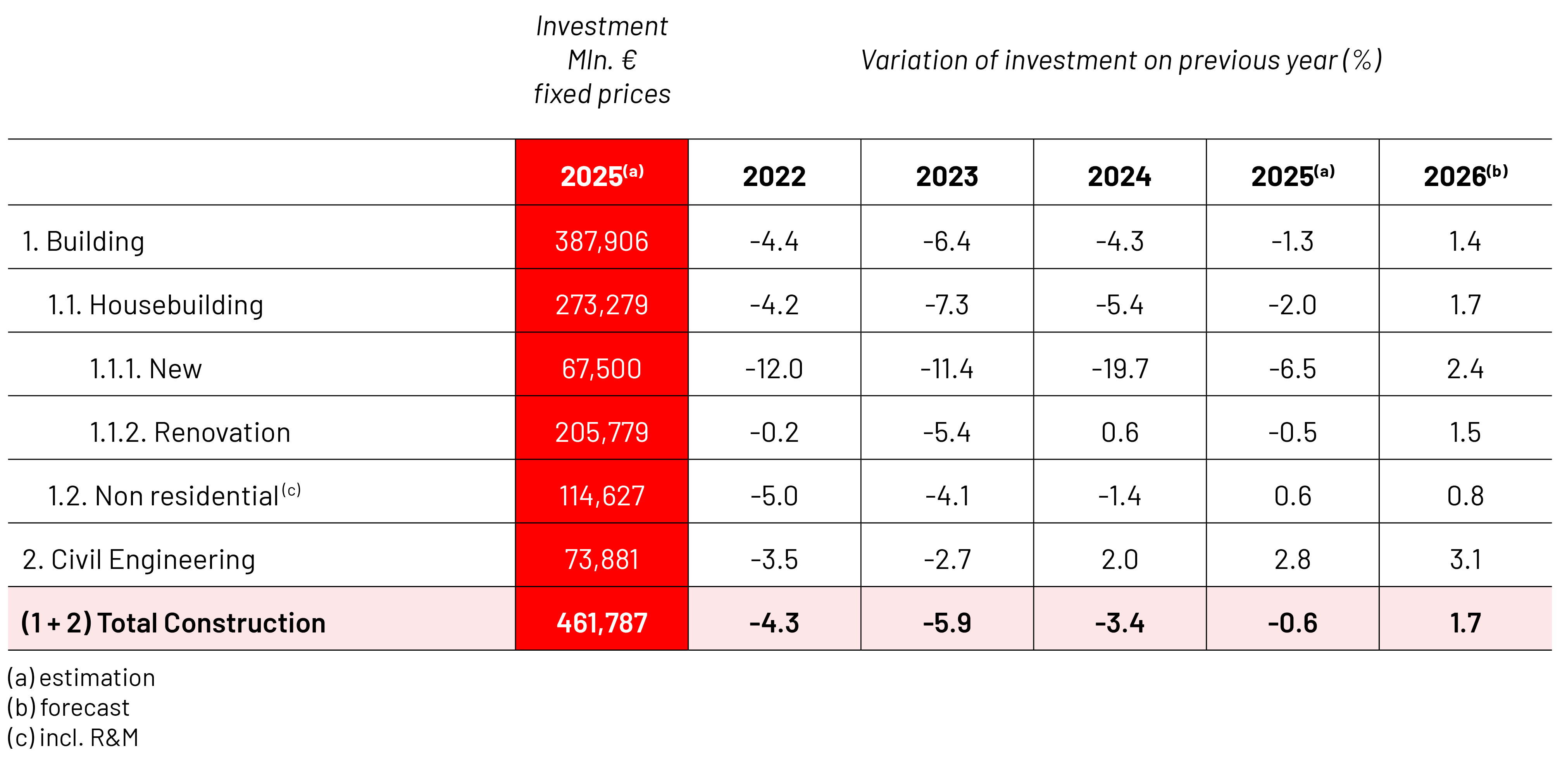

In 2025 the weak phase in the German construction sector continued. While real gross domestic product increased slightly by 0,2 %, construction investment fell by 0,6 % on a price-adjusted basis. At the same time, price adjusted turnover in the main construction sector increased by 2,4 % marking the first increase in five years. This contrasting development can be attributed to the fact that construction investment includes both the main construction sector and the renovation sector, which had not yet benefited from the rebound in construction demand in 2025, recording a decline of 3,3 %. Incoming orders increased by 6,8 % in real terms compared to the previous year and the order backlog rose by 10,2 %. However, the upward trend is not sufficient to offset the declines of recent years.

Due to the “Sondervermögen Infrastruktur und Klimaneutralität” and optimistic prospects for the housing sector, the overall outlook for the construction industry is slightly positive in 2026. Construction investment is likely to increase by 1,7 % in real terms, although developments will vary in individual construction sectors. Price adjusted turnover in the main construction sector is expected to grow by 2,5 %. However, the infrastructure fund largely replaces budget funds, and due to planning and procurement bottlenecks, it will not result in orders in the short term. Moreover, the forecast is subject to uncertainty, as the potential escalation of geopolitical risks in the Middle East are having an immediate impact on the development of material prices. In a survey conducted at the beginning of 2026, 52 % of construction companies identified energy and raw material prices as a risk to their business.

The construction labour market continues to show robust growth. Due to the increase in demand, construction companies slightly expanded their workforce by 0,7 % in 2025. For 2026, the increase is expected to continue rising by 1 %, or 10 000 workers, reaching a total of 933 000 people. For the first time, uniform wage rates have applied nationwide to employees in the construction sector in Germany since 1 April 2026. With the third phase of the tariff agreement, the decades-long wage gap between East and West Germany has been closed. Another achievement was the inclusion of apprenticeship wages that historically had even wider disparities. This harmonisation ensures uniform wage, competition, and working conditions nationwide in the German construction sector.

Housebuilding

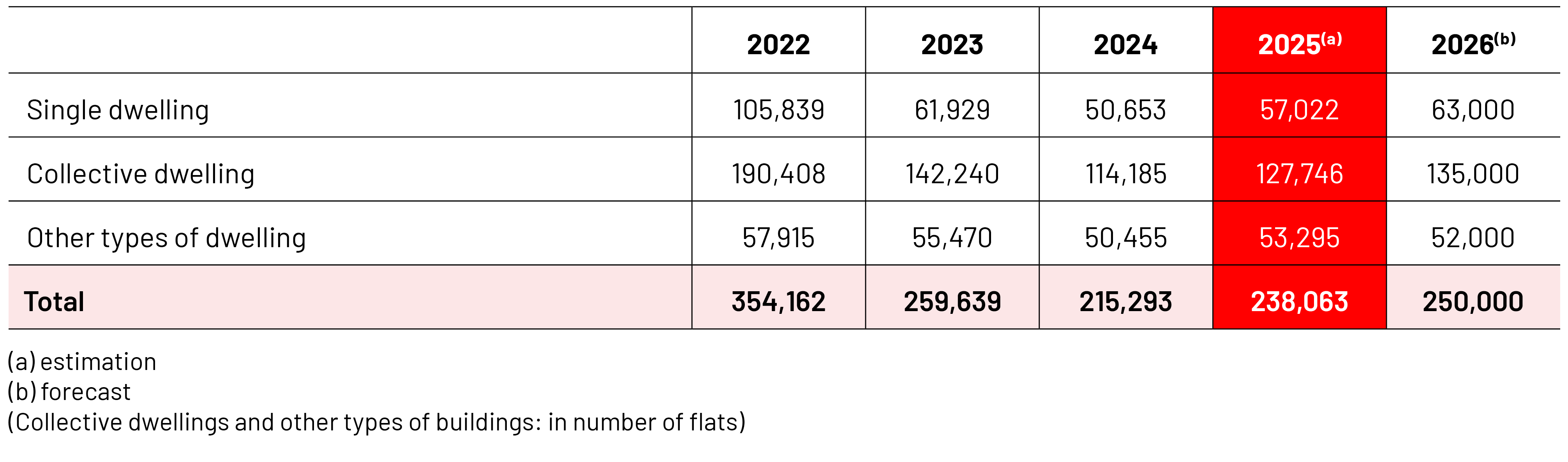

With a 60 % share of total construction investment, residential construction dominates the German construction sector. Its extremely weak performance over the last five years has therefore had a particularly strong impact on the overall construction market. In 2025 the downturn in residential construction continued. Turnover declined by 1,5 % in real terms. According to the Ifo survey, more than 40 % of companies still report a lack of orders. However, there are also positive signals for 2026: Incoming orders rose by 10 % on a price-adjusted basis, and the volume of new business for residential construction loans increased by 21 %. This is also reflected in the number of building permits, which increased by 10,8 % last year. The previous German government set a target of 400 000 new housing units per year. However, in 2024 only 252 000 homes were completed and in 2025 only 238 063 dwellings were permitted. Therefore, the number of completions is expected to continue declining in 2025 and 2026.

The government has set the goal of making Germany’s building stock climate-neutral by 2045. In order to achieve this, investment in energy-efficient renovation has to be significantly increased. While investment in existing residential buildings is likely to grow slightly in 2026 due to government subsidy measures and private investments, an increase in turnover for new residential construction by 2 % is to be expected.

However, two factors are having a negative impact. Interest rates for mortgage loans have risen from 1,3 % to over 4 % in just two years and remain at a high level. At the beginning of 2026 the interest rate was 3,7 %, which makes the financing of residential construction investments more expensive. Second, construction prices for residential buildings have risen by 34 % compared to 2021 mainly due to increased costs in materials. Under these conditions, many private households are unable to afford residential property.

Non-residential construction

80 % of non-residential building construction is accounted for by the commercial sector. Many investors – especially in industry – have put their investment plans on hold due to the weak economy, current developments in trade policy and declining exports. After a price-adjusted 10 % decline in orders in 2023, incoming orders fell by a further 8 % in 2024. In 2025 the non-residential building sector was dominated by large-scale projects for data centers. Therefore, incoming orders increased by 5,5 %. This trend is likely to continue in 2026.

Furthermore, funds from the defence budget are being spent on the construction of military barracks and funds from the “Sondervermögen” are being used for the construction of schools and childcare houses. Both are expected to have a positive impact on public building construction. Incoming orders increased by 4 % in 2025.

A stable trend is expected in the energy-efficient refurbishment of existing buildings. As energy prices remain at a high level, refurbishment measures are more profitable in the long term.

GDP 2025

BILLION

POPULATION 2025

Total investment in construction in 2025

BILLION

Civil engineering

This sector is dominated by the public sector, which accounts for around 80 % of investment in civil engineering. After years of neglecting transport networks, a turnaround can now be observed. This is reflected in the increase in orders due to several major projects in railroad and power line construction in the previous year. Deutsche Bahn AG, in particular, which is receiving considerably higher investment funding from the federal government, placed several large orders. In the public sector, however, road construction orders declined in 2025 despite a very high demand for road and bridge renovations. The 500 billion Euro infrastructure fund for investments over 12 years is expected to have a positive effect due to improved planning reliability. However, it is not provided in addition to the German Federal Budget. Instead, it mostly replaces funds that were previously cut from the federal budget. Therefore, the positive impact will be more limited than it was initially expected.

Prices of construction materials

The recent stabilization in prices observed for certain materials since February 2026 could soon come to an end due to rising oil and gas prices caused by the war in Iran. The price of diesel fuel has followed a largely sideways trend since autumn 2024, nevertheless the fuel price in February 2026 was 39 % higher than in January 2021. Some refineries have raised bitumen prices by 20 %. In addition to that, second-round effects are expected, causing particularly energy-intensive building materials, such as cement and asphalt, to become more expensive. In February, companies were already paying 48 % more for asphalt than at the beginning of 2021. This development is increasing cost pressure on construction companies, as diesel accounts for 41 % of total energy consumption in the construction industry. The average increase in construction service prices in 2025 was 2,8 %. For the current year, economic research institutes expect prices to increase by around 3,3 %.

Business registration and bankruptcy

The downturn trend of recent years is also reflected by insolvencies in the main construction sector. After peaking at 9 160 insolvencies in 2002, the number fell by more than three-quarters to 2 272 by 2021. By 2025, however, it had risen by more than half to 3 774 insolvencies.

Construction Activity

Number of building permits in residential construction