Overall construction activity

Ireland’s economy continued to expand through 2025, although the pace of growth moderated in response to global uncertainty and energy‑related inflation pressures. Modified Domestic Demand remained resilient throughout the year, supported by strong labour market conditions and sustained public investment. According to national accounts data, Modified Domestic Demand held up well despite global headwinds, and Construction Gross Value Added increased by 9.7% in 2025.

Total employment reached 2.83 million in late 2025, with unemployment stabilising at 4.7%. Construction employment also strengthened, rising from 176,600 in the final quarter of 2024 to 192,900 by the end of 2025 on a seasonally adjusted basis. Construction GVA grew by 9.7% during the year, and medium‑term projections indicate average annual growth of 4.8% between 2026 and 2029. This expansion was supported by ongoing public capital expenditure and improved activity across both building and civil engineering segments.

CSO production indices show that construction activity strengthened significantly during 2025. Civil engineering output surged early in the year, with a 16.6% increase in volume in the first quarter, while non‑residential building became the primary driver of growth later in the year, recording a 10.1% increase in the third quarter. Over the year as a whole, non‑residential building recorded a positive annual increase in production volume, whereas civil engineering activity was slightly negative on the CSO’s annual comparison, reflecting the inherent volatility of large infrastructure projects. Underlying investment in Gross Fixed Capital Formation is expected to continue expanding over 2025 and 2026, supported by public capital expenditure and housing investment, although at a more moderate pace in line with weaker global conditions.

Despite these improvements, construction output remains below the level required to meet Ireland’s structural housing and infrastructure needs. The CIF notes that sustained output growth will depend on accelerated delivery of key enabling infrastructure. New legislation coming into effect from mid‑2026 will require public bodies to cooperate, coordinate, prioritise and sequence their duties with other agencies, and to allocate the resources necessary, to ensure the rapid approval of major projects and programmes.

In summary, the Irish construction sector experienced a strong rebound in 2025, marked by significant growth in construction GVA, a 20% increase in housing completions, rising employment to almost 193,000, stabilising material cost inflation and continued expansion in civil engineering driven by public investment. However, structural constraints, including: planning delays, labour shortages, infrastructure deficits and viability challenges continue to limit the sector’s ability to meet Ireland’s long‑term housing and infrastructure needs.

The CIF emphasises that Ireland faces a ten‑year window before demographic pressures begin to significantly constrain fiscal capacity. Accelerating construction delivery during this period is essential to ensuring that Ireland can meet its economic, social and infrastructural objectives.

Housebuilding

Housing supply remains significantly below long‑term requirements, even though 2025 saw a strong increase in completions. A total of 36,300 new homes were completed during the year, representing a 20% increase compared with 2024. Quarterly completions ranged from 5,842 to 11,969 units, with the final quarter of 2025 marking the highest level of output.

A surge in commencements during 2024 carried into 2025, although the CIF cautions that this trend introduces forecasting uncertainty due to the influence of temporary policy incentives. The relationship between planning permissions, commencements and completions has become increasingly unstable, reflecting structural challenges across the delivery pipeline. Planning delays and regulatory complexity continue to impede progress, while infrastructure bottlenecks, viability pressures arising from construction costs and financing conditions, reduced institutional investment in the private rental sector, and persistent labour shortages all contribute to delivery constraints.

The CIF identifies five critical enablers required to support increased housing output: planning reform, enhanced financial supports, timely delivery of enabling infrastructure, greater adoption of Modern Methods of Construction, and reform of public procurement processes. Progress in these areas remains essential if Ireland is to close the gap between housing demand and supply.

Non-residential construction

Non‑residential construction activity remained below pre‑pandemic levels but showed clear signs of recovery during 2025. CSO data for 2025 indicates that the sector strengthened progressively through the year. The most significant improvement occurred in the third quarter, when non‑residential building recorded a 10.1% increase in production volume. This followed more moderate growth earlier in the year and reflects a shift in the composition of construction activity, with non‑residential building becoming the primary driver of output as the year progressed.

The recovery in 2025 was supported by stabilising market conditions and continued public and institutional investment. However, private sector development – particularly in the commercial office market – continued to face headwinds arising from tighter financing conditions, hybrid working patterns and existing capacity in the market. As a result, the improvement in non‑residential activity, while notable, remained uneven. Pipeline visibility, funding conditions and evolving demand patterns will continue to shape activity levels in the short to medium term.

GDP 2025

BILLION

POPULATION 2025

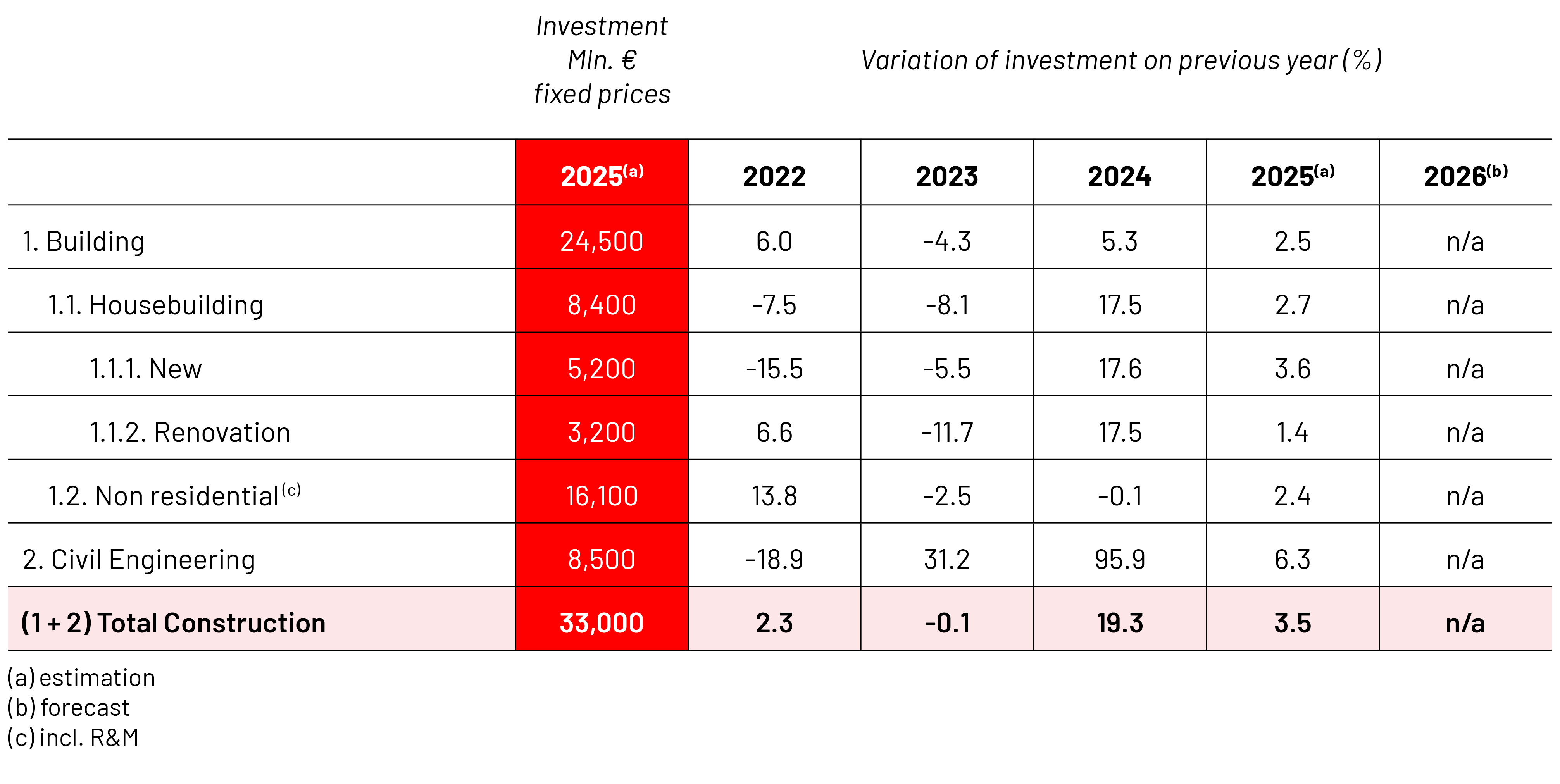

Total investment in construction in 2025

BILLION

Civil engineering

Civil engineering remained a central and stabilising component of the construction sector in 2025, driven primarily by public investment under the National Development Plan. CSO production index data for 2025 shows that civil engineering output experienced a strong surge early in the year, with a 16.6% increase in volume in the first quarter. This early momentum reflected the advancement of several large infrastructure projects and the continued prioritisation of public capital programmes.

However, this surge was not sustained throughout the year. Civil engineering activity moderated significantly in subsequent quarters, and by the time annual comparisons were made, the sector recorded a slight decline in output relative to the previous year. This pattern reflects the inherent volatility of large‑scale infrastructure delivery, where quarterly output can fluctuate depending on project sequencing, procurement timelines and the mobilisation of major works.

Despite this variability, civil engineering remains underpinned by a substantial pipeline of public investment, with €102.4 billion allocated for the period 2026–2030. Delivery challenges persist, including staffing constraints within public bodies, delays in planning and procurement processes, and regional infrastructure deficits in water, wastewater and transport. Addressing these issues remains essential to ensuring that civil engineering output can expand in line with national requirements.

Prices of construction materials

Although inflationary pressures eased somewhat during 2025, the construction industry remains exposed to significant cost volatility as the Irish economy continues to experience the effects of global energy shocks, particularly those linked to the Iranian conflict. The resulting spike in fuel costs has placed considerable pressure on construction companies, especially given the fuel‑intensive nature of producing key materials such as cement, concrete and steel. These increases have compounded an already challenging environment in which a large majority of CIF members report concerns about raw material costs. As a small island economy, Ireland faces additional cost pressures due to transport and logistics, and the industry is now experiencing broad‑based price increases.

These pressures are having a direct impact on construction costs across all segments of the sector. The cumulative effect of sustained cost increases over recent years continues to undermine project viability, particularly in the residential market. The re‑emergence of cost pressures in 2026 remains a significant concern for the industry.

At the time of writing, wholesale prices for building and construction materials increased by 1.7% in the 12 months to March 2026, although this index does not yet reflect the more recent increases associated with the Iran conflict. A significant rise is expected in the next statistical release due at the end of May 2026. Notable increases over the past year include copper pipes and fittings (6.9%), plaster (6.7%), ready‑mixed concrete (4.8%) and rough hardwood timber (4.6%). The Building and Construction Index increased by 2.4% in the year to March 2026.

Construction Activity

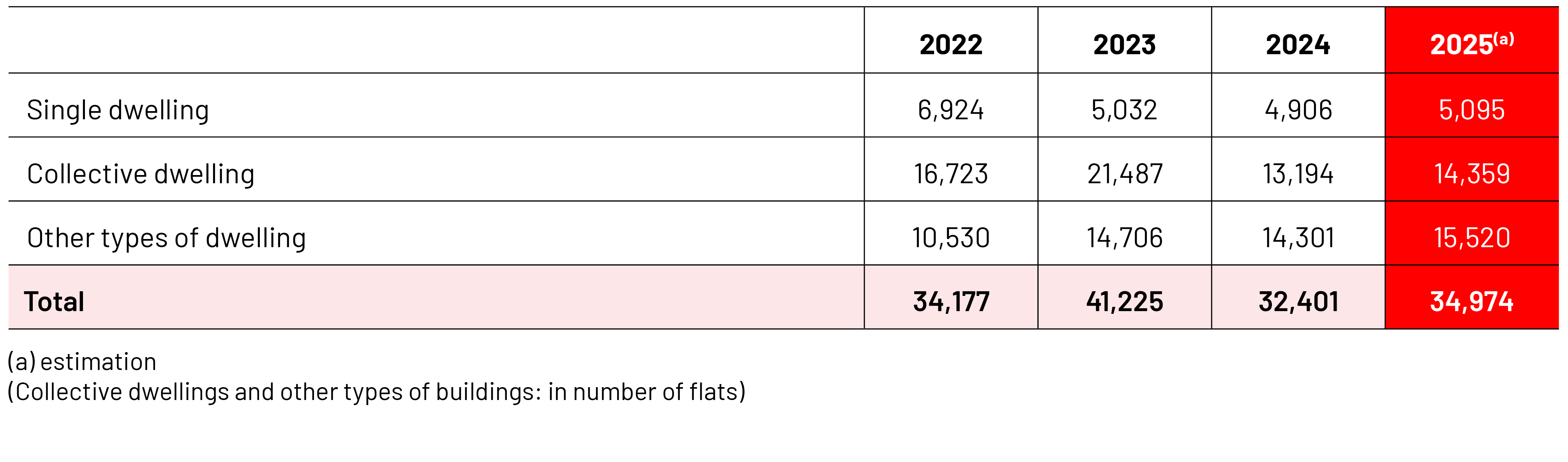

Number of building permits in residential construction