Overall construction activity

In 2025, construction activity continued to play a key role in the Spanish economy: in terms of Gross Fixed Capital Formation it represented 10,8% of GDP, in terms of Gross Value Added it represented 5,4% of GDP.

Factors that mainly conditioned construction activity in 2025 were the impulse in public tendering for works, the increase in the number of “visados” and the upward trend in housing segment -both in new construction and renovation- although lower than sectoral expectations, the low level of public tendering for concessions, and the challenge of labour shortage that limited in general the capacity of companies to deploy all their potential. The positive impact on our country of the European NextGenerationEU recovery funds must be also mentioned, even if the implementation rhythm was not as agile as initially foreseen, particularly in dwelling and dwelling/building renovation areas.

From the perspective of employment, the sector had 1,47 million workers in 2025, an increase of 3,1% in comparison with 2024. Women accounted for 11,5% of the total figure, representing the highest percentage share in the last ten years. Foreign workers represented 20,7% of the total, of which 71% were non-EU nationals. As it was noted in the latest report, one of the main concerns in the sector is the shortage of labour and the ageing of the active population without generational replacement. Only 10,8% of workers in the sector are under 30 years old, while the percentage of workers over 55 years old reaches 22%. Furthermore, there is a slow but steady increase in the average age, which now stands at 45,1. On the other hand, the proportion of young workers has been stagnant for a decade, rising by just 1,3 percentage points since 2015, whilst the proportion of workers aged 55 and over has increased by 8,6 percentage points.

Another interesting sectoral data is usually the apparent cement consumption, as a leading indicator of production; 2025 showed an increase of 11,55%, rising for the second consecutive year and reaching its highest level in the last ten years. It peaked in October and exceeded 2024 levels in every month except April, due to the calendar effect.

In relation to the regulatory framework, once again from the CNC must highlight that price revision in public contracts is still a pending issue in the Spanish Law on Public Sector Contracts. As already explained in the latest report, it is essential to guarantee the economic re-equilibrium of public contracts in order to cope with the unexpected increases in the prices of energy, materials and wages. The fact that in our country companies cannot act by applying appropriate price revision clauses is having a negative impact on their competitiveness, if we compare the situation with other Member States where companies do have mechanisms to address this issue to a greater or lesser degree. The absence of price revision and, in addition, the fact that many public contracts are tendered at non-updated prices, have led in recent years to an increase in the number of tenders that do not receive any offer or tenders where there is only a single bidder. The CNC continues to call on the Government to adopt an appropriate system of price revision in public contracts; the current conflict in the Middle East and the subsequent rising the prices of energy and different materials, have made evident the shortcomings of our legislation, which lacks adequate price revision mechanisms.

In this section dedicated to presenting the panorama of the sector, the issue of housing must be specifically tackled, as it was last year. In our country, there is an urgent need to increase the creation of housing. The construction of at least 220 000 homes per year would be required to respond to the current housing shortage, which could reach a deficit of 2,74 million in 2039 if annual production does not considerably increase.

To conclude and regarding forecasts for 2026, recent short-term indicators suggest that Spanish economic activity would continue to grow in 2026 but with the forecast of a gradual slowdown in the growth of activity. According to the macroeconomic projections published by the Bank of Spain in March this year, GDP growth is expected to stand around 2%-2,2% in 2026, and 1,8% in 2027. However, these projections are conditioned by the uncertainty arising from international trade and geopolitical tensions. As for the sector, a relevant increase in residential construction activity is expected due to Government's commitment to address the problem of housing shortage; non-residential construction would register more attenuated growth and civil engineering works tendering is expected to decrease in comparison with 2025 once contracts funded under the Recovery Resilience Facility-NextGenerationEU have already been awarded.

Housebuilding

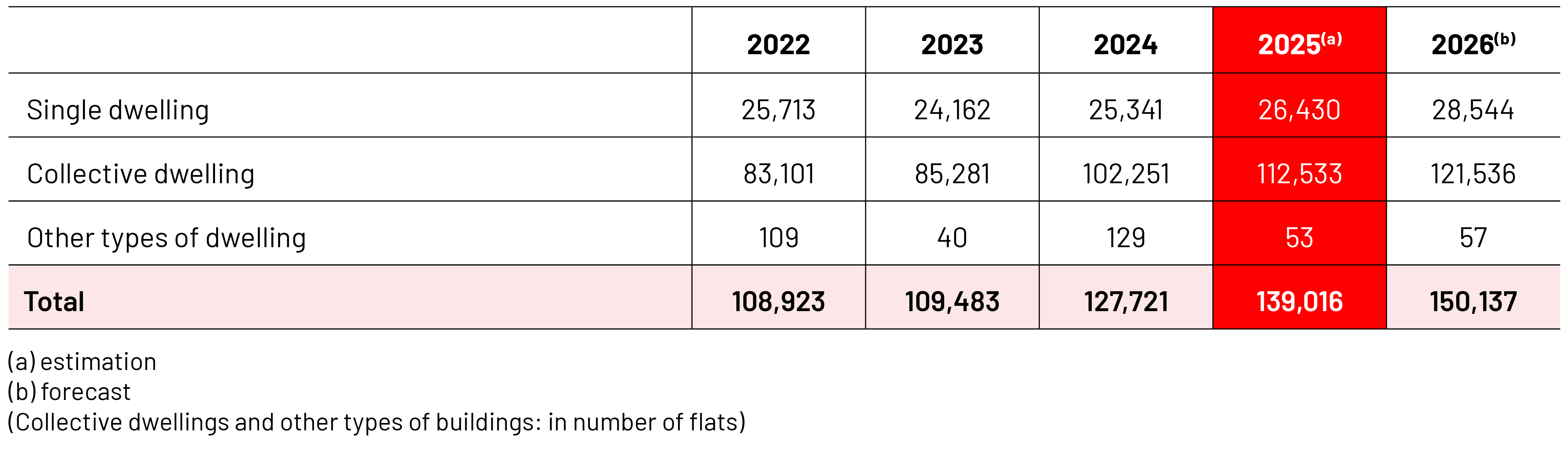

The number of “visados de dirección de obra” in terms of new dwellings in 2025 stated at 139 016, +16,7% in comparison with last year. Despite this, and as noted in a paragraph above, this trend is insufficient to respond to housing needs. In order to enable the increase of housing offer, it is essential to streamline the transformation and management of land, improve the permitting process, reduce considerably the current taxation burden on housing, promote public-private partnerships to develop projects and guarantee a workable public funding allocation for boosting housing policies. Recently this year, the Government has approved a new National Housing Plan for the period 2026-2030; therefore, new housebuilding should keep an upward trend in the coming years.

The role that industrialised construction may have in contributing to fostering the supply of housing must be also mentioned. In in this respect, the Government launched in 2025 the Strategic Project for Economic Recovery and Transformation (PERTE) for the Industrialisation of Housing, that will contribute to the transformation and efficiency of construction.

With regard to the renovation segment, as explain in the latest report, the national Recovery and Resilience Plan has allocated around 10% of its budget to an ambitious renovation and urban regeneration action, where residential renovation, linked to the improvement of energy efficiency, is one of the priorities. In 2026 results should speak. The National Housing Plan recently adopted, also includes measures to foster renovation

Non-residential construction

In 2025, this segment was driven by the relevant increase recorded in the volume of public tenders. In 2026 this positive trend would continue, mainly based on public tendering for social equipment such as in the area of health and sports.

GDP 2025

BILLION

POPULATION 2025

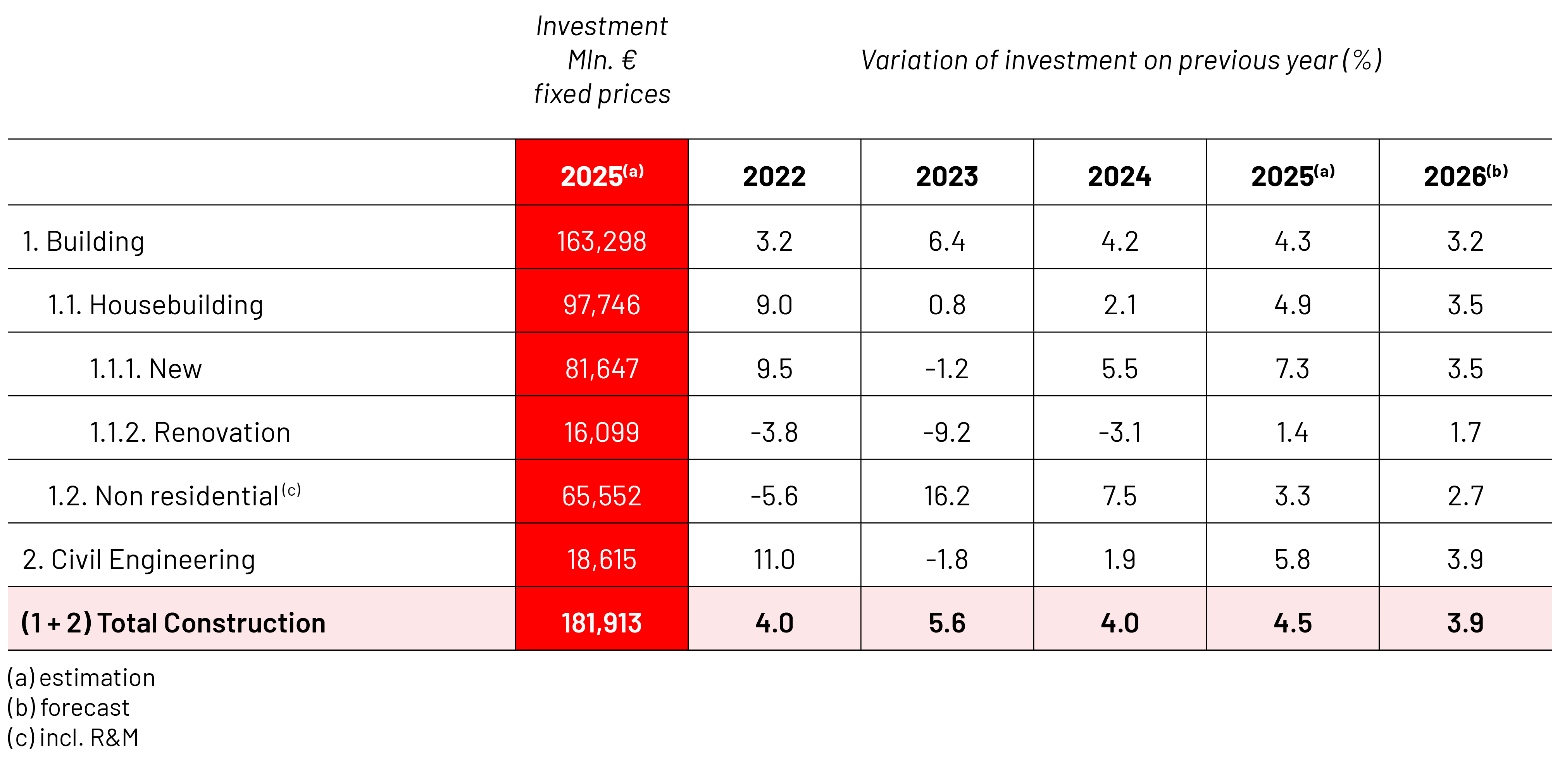

Total investment in construction in 2025

BILLION

Civil engineering

In 2025, the volume of public tenders in civil engineering amounted to € 18 615 million notably because of the investments included in the national Recovery and Resilience Plan; railway and road projects received the largest share of the investment.

However, an investment deficit in public civil engineering works and maitenance has been noticed since 2011. The stimulus provided by the Plan for the period 2021-2025 has alleviated to some extent that situation, but the investments that the country needs mainly in sustainable mobility, water and environment and energy, including maintenance of infrastructures, requires that the budgetary insufficiency over the last decade on the part of the Public Administrations, prior to the RRF, may be reversed to enable a sustainable upward investment trend.

Prices of construction materials

Unfortunately, at the time of writing this note, the National Statistics Institute has not published yet price indices covering the entire year 2025; there are only data available up to Q3 2025. Additionally, the starting point for filling the FIEC table is Q1 2023 and the table does not reflect what is happening right now. For these reasons, it is important to broaden the picture in relation to this issue. Considering the period 2021-2025, energy increased 29%, cement 47,1%, bitumen 25%, aluminium 33% glass 28,4% or steel 15,6%. This year, since the outbreak of the conflict in the Middle East, sharp increases in the prices of energy, gas, brent crude, bitumen, aluminium or steel have occurred.

Business registration and bankruptcy

The number of bankruptcy proceedings in construction in 2025 was 925 increasing by 7,7% in comparison with 2024.

Regarding business registrations, at the time of writing this note according to available data referred to 1 January 2025, it could be said that the net number of new businesses in the sector was 5 524 comparison with 2024 (including physical persons, public limited companies, limited liability companies and other legal forms).

Construction Activity

Number of “Visados de dirección de obras”- number of new dwellings