Overall construction activity

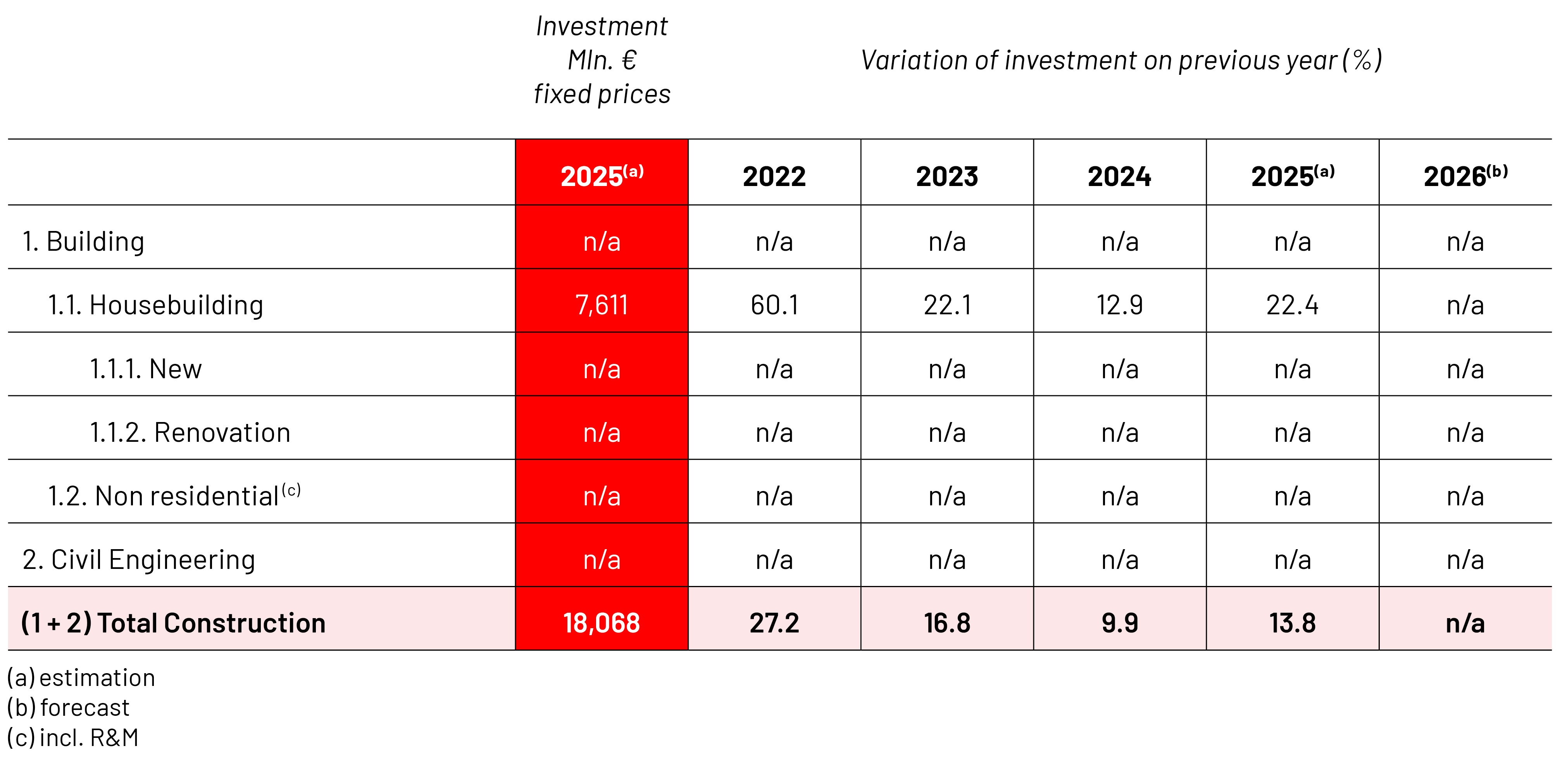

In 2025, the construction sector continued its strong expansion within a favourable macroeconomic environment. Construction investment reached EUR 18.07 billion, accounting for approximately 7.3% of GDP, (which reached EUR 248.35 billion at current prices), while gross value added increased to EUR 5.27 billion from EUR 4.57 billion in 2024 (+15.3%). Gross fixed capital formation rose to EUR 15.12 billion in constant prices (+16.6%), confirming sustained growth in real construction activity.

Labour market conditions remained supportive, with construction employment increasing to 707,628 persons (out of a total national employment of 4.34 million). At the same time, labour shortages became increasingly evident, particularly in skilled occupations, creating capacity constraints for the sector. Despite strong market conditions, geopolitical uncertainty, particularly related to developments in the Middle East, may affect construction costs, investment sentiment and overall market activity. The impact on the Greek construction sector will depend on the duration and intensity of these developments.

Business activity remained positive, with 9,568 new company registrations reflecting continued confidence in market prospects. However, bankruptcies increased to 43 firms, highlighting the challenges posed by labour shortages, elevated costs and increasing competition. These developments indicate a more selective market environment, favouring financially stronger and more efficient companies.

Construction material prices continued to rise, although at a slower pace than during the inflationary period of 2021–2023. While inflationary pressures have eased, material costs remain structurally elevated, continuing to affect contractors' margins and project costs.

For 2026, construction activity is expected to remain positive, although growth is likely to moderate as investment dynamics mature and supply-side constraints become more pronounced. Market consolidation is expected to continue, while elevated construction costs and geopolitical uncertainty may continue to affect project affordability and investment decisions.

Housebuilding

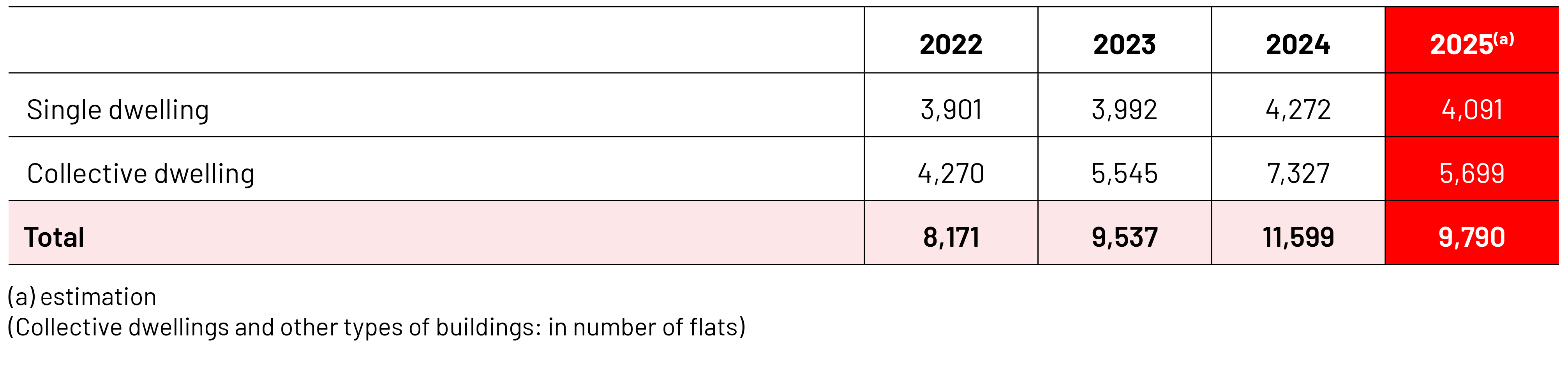

In 2025, residential construction recorded strong growth, with investment increasing to EUR 7.61 billion from EUR 6.07 billion in 2024 (+25.4%). In real terms, residential investment reached EUR 6.36 billion, confirming continued expansion in construction activity. At the same time, residential building permits declined to 9,790 units from 11,599 units in 2024 (-15.6%). Single dwellings fell to 4,091 units, while collective dwellings declined to 5,699 units, suggesting that current activity is largely supported by projects already in the pipeline. Collective dwellings remained the dominant housing type, reflecting continued demand for higher-density urban developments.

The residential property market continued to attract domestic and foreign investors, although at a more moderate pace than in previous years. Demand remained stronger than the supply of modern and affordable housing, supporting further increases in house prices. The subsidised housing programme “Spiti mou II” also continued to support market activity. Construction costs continued to rise, although at a slower pace. According to ELSTAT, the Material Price Index for new residential buildings increased by 2.5% in February 2026, compared with 4.0% a year earlier, indicating a gradual easing of cost inflation.

For 2026, residential investment is expected to remain positive, although the weakening permit pipeline may gradually constrain new supply. Housing market pressures are therefore expected to persist, supporting house prices and investment in high-quality, energy-efficient residential properties.

Non-residential construction

In 2025, non-residential construction continued to benefit from strong investment activity, with gross fixed capital formation reaching EUR 15.12 billion in constant prices (+13.8%). Price increases and investment demand remained concentrated in premium office space, tourism/hospitality assets, and logistics/warehousing, though growth moderated compared with previous years. This sustained activity was heavily anchored by EU funding, particularly through the Recovery and Resilience Facility (RRF).

For 2026, non-residential construction is expected to maintain positive growth, supported by continued EU fund absorption and resilient investment demand, although activity is likely to moderate as private investment conditions become more challenging.

GDP 2025

BILLION

POPULATION 2025

Total investment in construction in 2025

BILLION

Civil engineering

Civil engineering remained a key pillar of construction activity in 2025, supported by major public infrastructure projects and EU co-financing programmes. The sector continued to play an important role in improving transport and network infrastructure, contributing to broader economic development.

However, leading indicators point to some moderation in momentum, with the construction production index increasing by 2.5% in 2025, compared with 19.9% in 2024, indicating continued but slower growth. At the same time, project implementation may face challenges from supply-chain disruptions and higher costs for key materials such as steel and aluminium.

For 2026, large-scale infrastructure projects are expected to remain on track, supported by ongoing public investment programmes and EU funding, providing continued support to civil engineering activity.

*Data being extracted by National Statistical Authority of Greece (ELSTAT) as well as the Bank of Greece Governor’s Annual Report

Prices of construction materials

In 2025, construction material prices show a transition from high inflation volatility to a more stable but structurally elevated cost environment. Index levels remain above the 2023 base (Q1 = 100), with steel at approximately 104, cement at 112, bitumen at 113 and wood at 114.

Although the pace of increase has moderated compared to the 2021–2023 inflationary period, the key structural feature is the persistence of elevated price levels relative to the base year. This indicates that the sector is not experiencing full price normalization, but rather a re-pricing at a higher equilibrium level.

The implication is twofold. First, nominal construction investment is mechanically supported by higher input costs. Second, real margins are compressed, particularly for smaller contractors and fixed-price contractual arrangements, increasing sensitivity to cost overruns and procurement efficiency.

However, according to Hellenic Statistical Authority (ELSTAT) the Overall Material Price Index in the Construction (CSTM) of New Residential Buildings with base year 2021=100.0 in February 2026 recorded an increase of 2.5% in comparison with February 2025. The corresponding index in February 2025 had recorded an increase of 4.0% compared with February 2024. The graph on the side shows that while in 2021 and 2022 the prices where escalating, during the years 2023-2024-2025 the increase of the prices somehow deescalated.

For 2026, structural elevation of costs, along with the energy and shipping logistics rise of costs due to the ongoing war in the Middle East, will continue to constrain affordability in housing and reduce elasticity in project initiation.

Construction Activity

Number of building permits in residential construction