Overall construction activity

The construction activity in 2026 is set to experience moderate growth after a relatively weak performance in 2025. The sector is expected to rebound, driven by decreasing interest rates, rising real wages, and significant public investments. Despite the downturn in recent years, construction employment remains high. Activity levels are predicted to increase by 2,200 personnel in 2026, with further however slighter increase of 700 employees in 2027, primarily due to increased public building and civil engineering investments. The professional construction activity, inclusive of maintenance, renovation, and new projects, indicates a less aggressive expansion for 2026, reflecting a cautious yet positive outlook.

Housebuilding

The housebuilding sector has shown considerable volatility. It reached a peak in 2022 with about 39,000 new homes but saw a significant drop to 24,000 in 2023. This decline is attributed to higher interest rates and inflation, which constrained borrowing and reduced housing market activity. There is an increase in residential construction in 2024, with around 31,600 new homes initiated, reflecting that 2023 stands out as a year with a low number of residential constructions. However, as interest rates are anticipated to decrease, the number of new housing starts is estimated to rise modestly to 33,200 in 2025 and to 33,600 in 2026. The falling interest rates and recovering real wages are expected to revitalize housebuilding investments, reversing the prior downturn and supporting gradual growth.

Non-residential construction

The non-residential building sector is projected to experience a small increase in 2026. The sector has been increasing slowly over the years, contingent on improved financial conditions and increased industrial production outside the pharmaceutical industry. The anticipated decline in interest rates is likely to spur renewed industrial and commercial building investments, with projections indicating a 2,1% growth in 2026. The upturn is expected to be short as the commercial building investments are projected to decrease with 2,9% in 2027. This decline reflects the fact that some of the large-scale building projects are expected to be finished during 2027.

GDP 2025

BILLION

POPULATION 2025

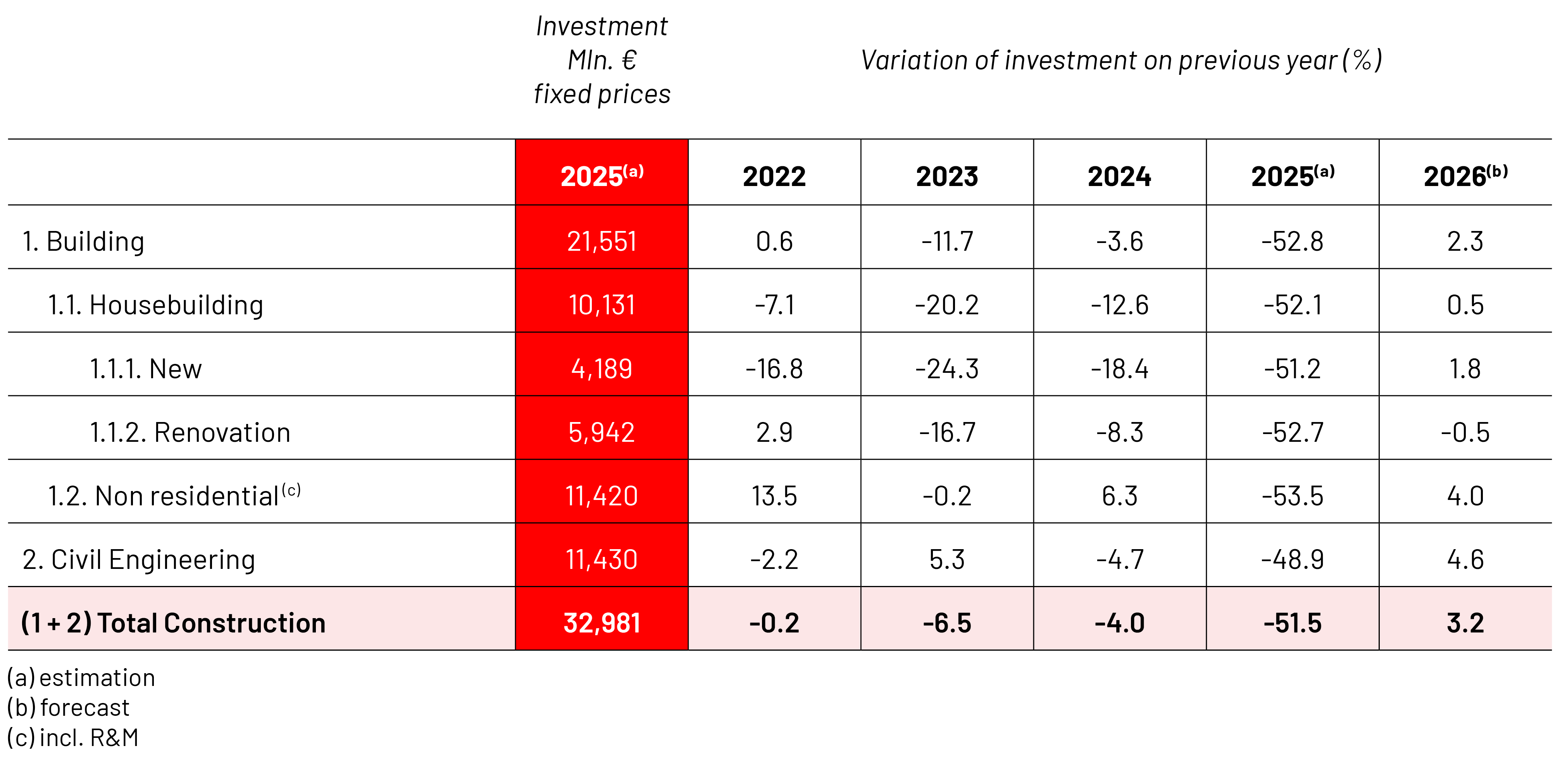

Total investment in construction in 2025

BILLION

Civil engineering

Civil engineering activities continue to show robust growth, supported by ongoing large-scale projects like the Femern Belt connection, Lynetteholm, and infrastructure upgrades under the Infrastructure Plan 2035. This sector remains resilient, buoyed by substantial long-term investments in green energy transformation, including fjernvarme (district heating) and enhancements to electricity grids necessary to meet ambitious climate goals. The sustained high level of activity from these projects ensures positive growth contributions through 2026 in current market prices. Anticipated growth rates within civil engineering are predicted 5,8% in 2026 and 7.1% in 2027, underscoring the durability of this sector's expansion and its pivotal role in maintaining high employment levels within the construction industry. Public sector investments have been critical, with forecasted change of 7.5%, and 14.5% in 2026, and 2027 respectively.

Prices of construction materials

Between Q1 2023 and Q4 2025, construction material prices showed varying trends. Steel prices peaked in Q1 2023 with the base index of 100 and consistently declined to 78 by Q4 2025. Cement prices steadily increased from 100 to 107 by Q4 2025, with slight fluctuations. Bitumen saw a peak at 104 in Q3 2023 but dropped to 76 by Q4 2025. Wood prices remained relatively stable compared to the other materials, with the lowest price at 95 during 2024 but increased to 97 in Q4 2025.

Business registration and bankruptcy

Between 2021 and 2025, business registrations and bankruptcy declarations showed some contrasting trends over the year. Business registrations decreased from 3,500 in 2021 to 2,510 in 2025, indicating lower entrepreneurial activity. Conversely, bankruptcy declarations increased from 1,190 in 2021 to a peak of 1,280 in 2023, however declined to 1,060 in 2025.

Construction Activity

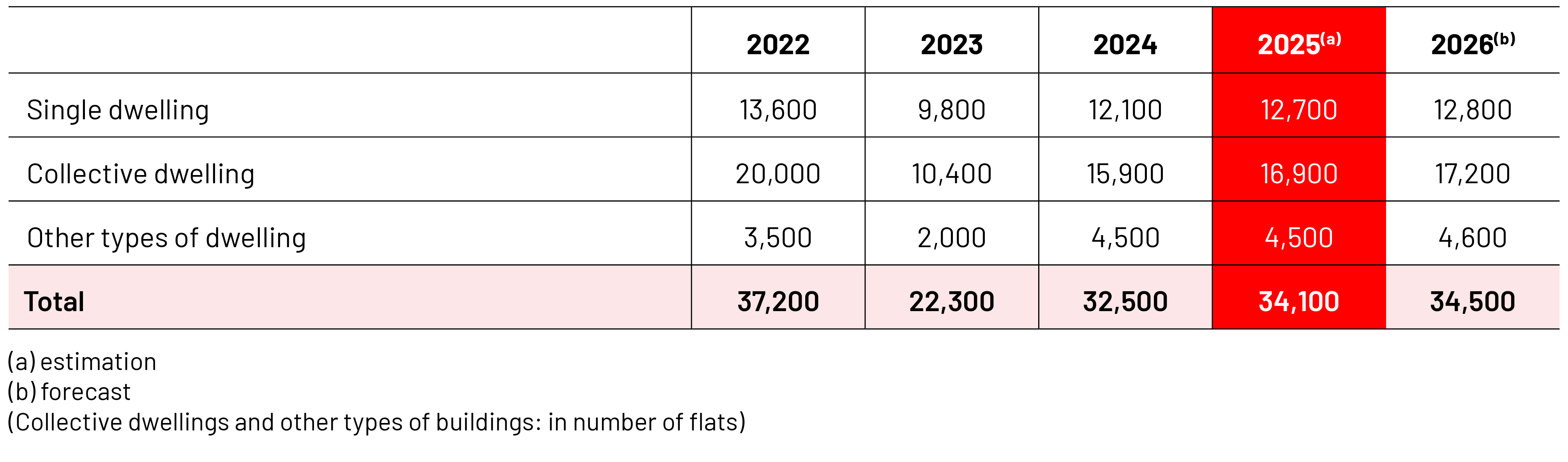

Number of building permits in residential construction