Overall construction activity

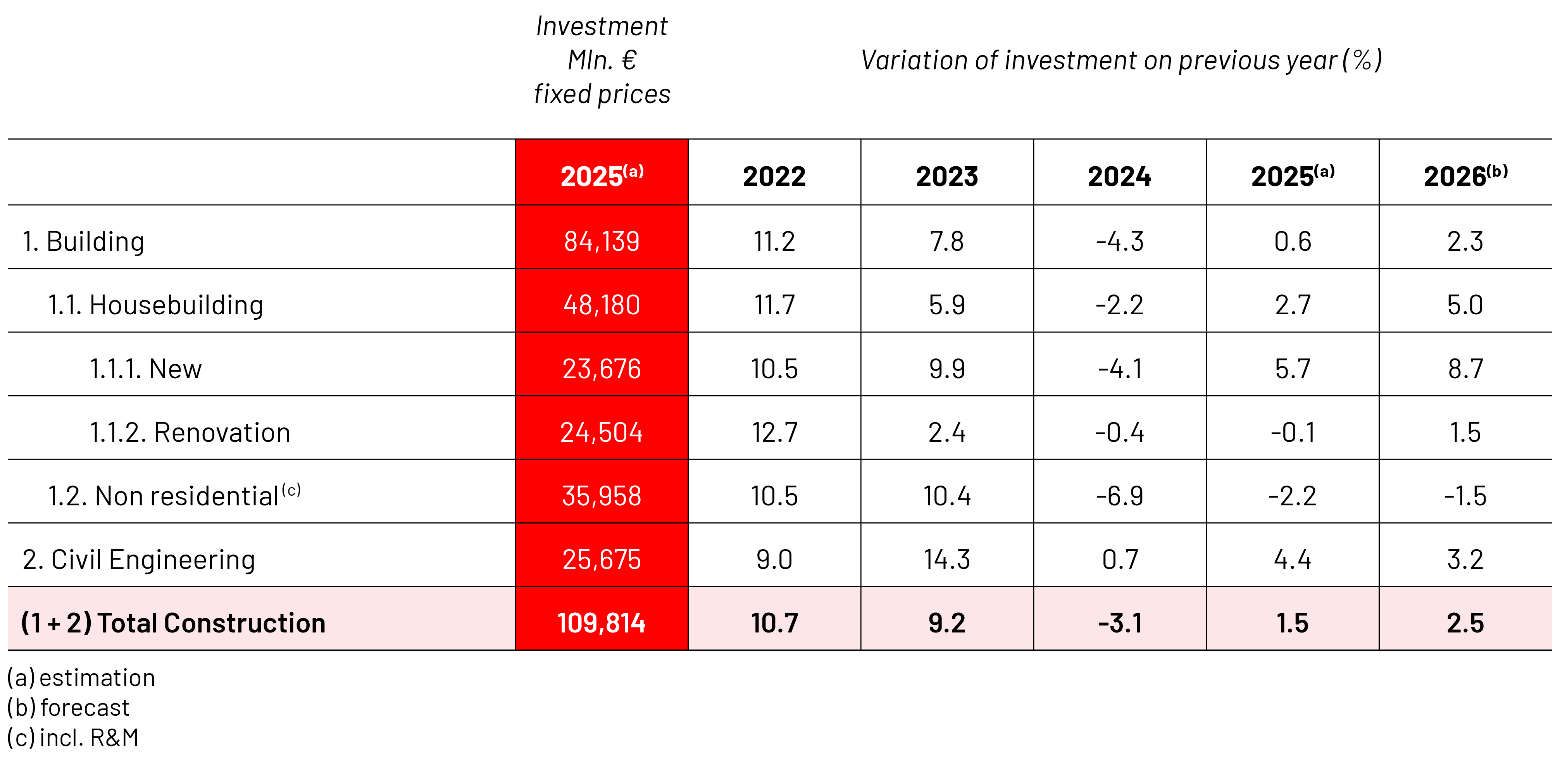

After a year of contraction, overall construction activity showed moderate growth of 1½% in the past year. This growth was predominantly observed in new residential construction, which increased significantly due to a rise in buildings permits issued in 2024. Civil engineering showed strong growth of production volume as well. Especially grid companies and water authorities invested significantly to address big challenges regarding grid congestion, flood protection and water safety.

The outlook on overall construction activity is expected to improve significantly this year. The total construction output by volume will grow by 2½% in 2026. Key drivers of this expected growth include the increase in granted permits for residential properties as well as the substantial investments in both improving the water system and strengthening the energy grid.

Residential construction

After a decline in production in 2024, residential construction increased by 2½% in 2025. The production growth was mainly the result of a strong increase in building permits in previous years. The growth of new residential construction is expected to persist more strongly in 2026. The number of completed dwellings is projected to rise to 80,000 in 2026 due to high levels of permit issuance in previous years. Demand for housing remains consistently high during this period due to continued supply shortage and household growth in the Netherlands. The rising housing prices particularly provide the financial capacity for developers to build more residential property. Although the number of completed dwellings is expected to rise over time, it will not be sufficient to reach the government’s target of 100,000 new dwellings per year.

After years of high growth, the renovation of residential properties decreased by 1% in 2025. This decline is mainly due to the saturated demand for sustainable improvements in both individual and multi-family dwellings. Particularly the demand for solar panels and heat pumps fell in 2025. In 2026, residential renovation is expected to slightly rise again. This growth is mainly the result of government policies that aim to phase out gas use in both new and existing dwellings.

Non-residential construction

Non-residential construction decreased by 2½% in 2025. This overall decline in output was partly caused by reduced retail consumption, resulting in limited construction of new shops by retail chains. Furthermore retail vacancy increased as fewer shops have been transformed to alternative uses. In addition, a decline in new agricultural construction took place over the past year due to production constraints related to phosphate and nitrogen regulations as well as the uncertain long-term outlook for farmers with national policies aiming 50% reduction of livestock. In 2026, construction of new non-residential buildings is expected to sharply decline as well. The decline is mainly concentrated in the construction of business premises, logistic facilities and offices.

After a contraction in 2024, renovation of non-residential properties slightly increased in 2025. The growth was mainly driven by increased subsidies (DUMAVA) to make educational and other public-sector properties more sustainable. In offices, however, renovation activity declined as the sustainability stimulus from the mandatory energy label C requirement faded. Besides that normalisation towards lower gas prices, feed-in costs for solar panels and grid capacity constraints had downward pressure on non-residential renovation activity. In 2026, renovation of non-residential properties is expected to slightly increase as efforts to improve sustainability will continue to rise.

GDP 2025

BILLION

POPULATION 2025

Total investment in construction in 2025

BILLION

Civil engineering

After a year of slight contraction, the civil engineering sector has strongly increased by 4½%. This growth was broadly supported by the different contracting parties in civil engineering. Grid operators significantly increased investments in strengthening and expanding grid capacity, while water authorities increased investments to strengthen the water system in light of new regulations (KRW). Construction activity on behalf of decentralised authorities also rose to prepare new housing sites for construction.

In 2026 construction activity in civil engineering will continue to grow at a more moderate pace. Investments by grid operators and water authorities are expected to increase, whereas civil engineering activity by the central government will slightly decrease due to the absence of price adjustment on existing budgets to cover increasing costs.

Prices of construction materials

The prices of construction materials show different patterns in 2025. The prices of construction materials have all increased in the first half of 2025. In the second half of 2025 both steel and bitumen prices decreased, while the prices of cement and wood stabilized. Especially the price of wood has significantly increased compared to previous years, whereas the price of cement is lower than in 2023 and the first half of 2024.

Construction Activity

Number of building permits in residential construction