Overall construction activity

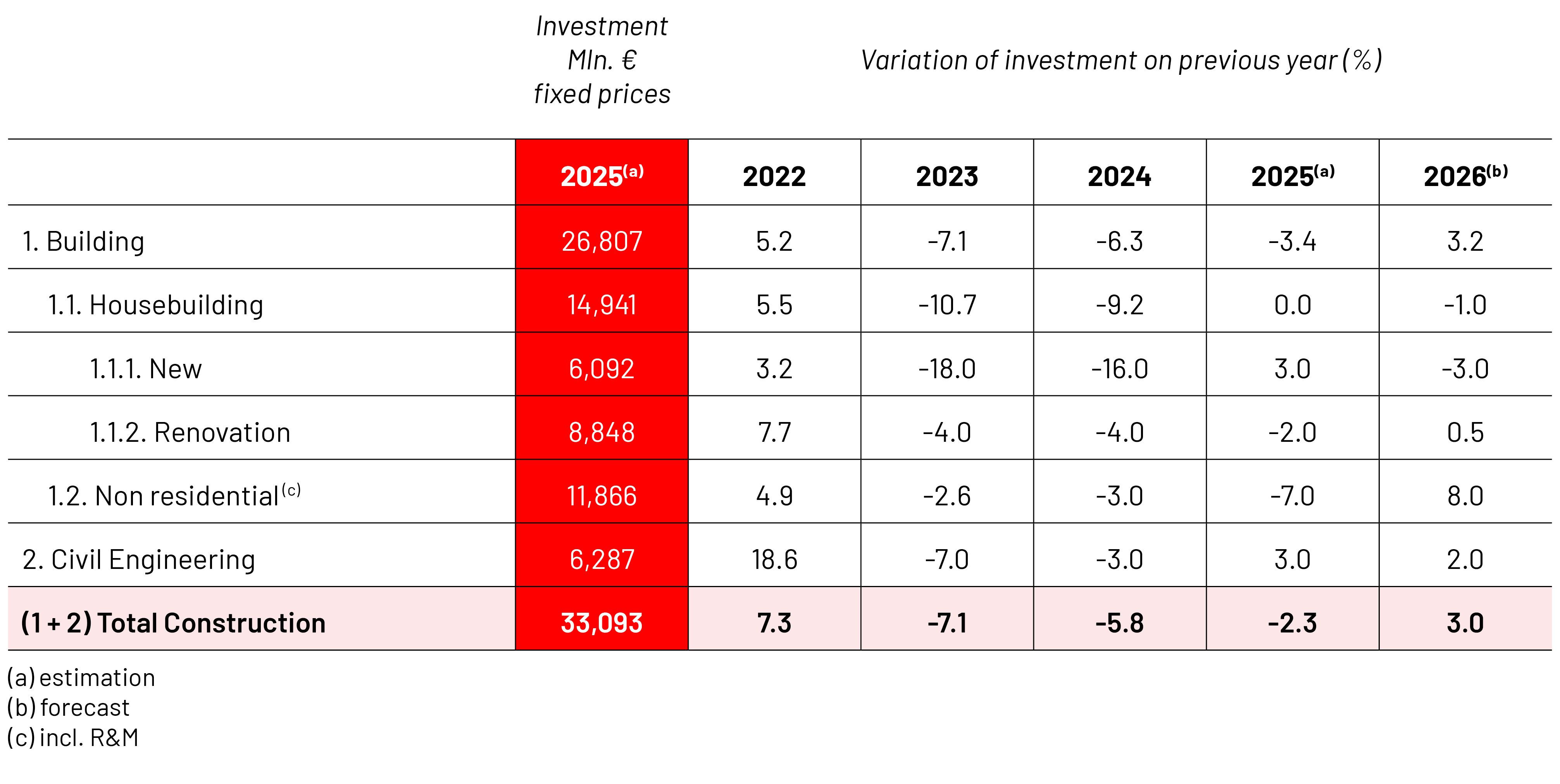

The decline in construction continued last year, although clearly more slowly than in previous years. Investments in residential construction grew by one percent thanks to a strong surge in subsidized housing production toward the end of the year. Investments in non-residential construction, however, remained one percent in the negative following the spring tariff disputes. Turnover increased due to the higher number of completed projects.

The number of new building construction starts continued to decline by just under three million cubic meters to a record low level of 25 million cubic meters. However, building permits — which indicate future production — remained at the previous year’s level of 30 million cubic meters.

The volume of new construction fell by 5 percent due to the sharp contraction in non-residential construction. Renovation activity returned to growth at the end of last year after nine consecutive negative quarters. Civil engineering is estimated to have grown steadily. Employment increased slightly despite the decline in construction volume. The turnaround in material deliveries to construction sites during the latter half of last year gave hope for a genuine recovery in construction activity. However, deliveries continued to decline at the beginning of this year.

Housebuilding

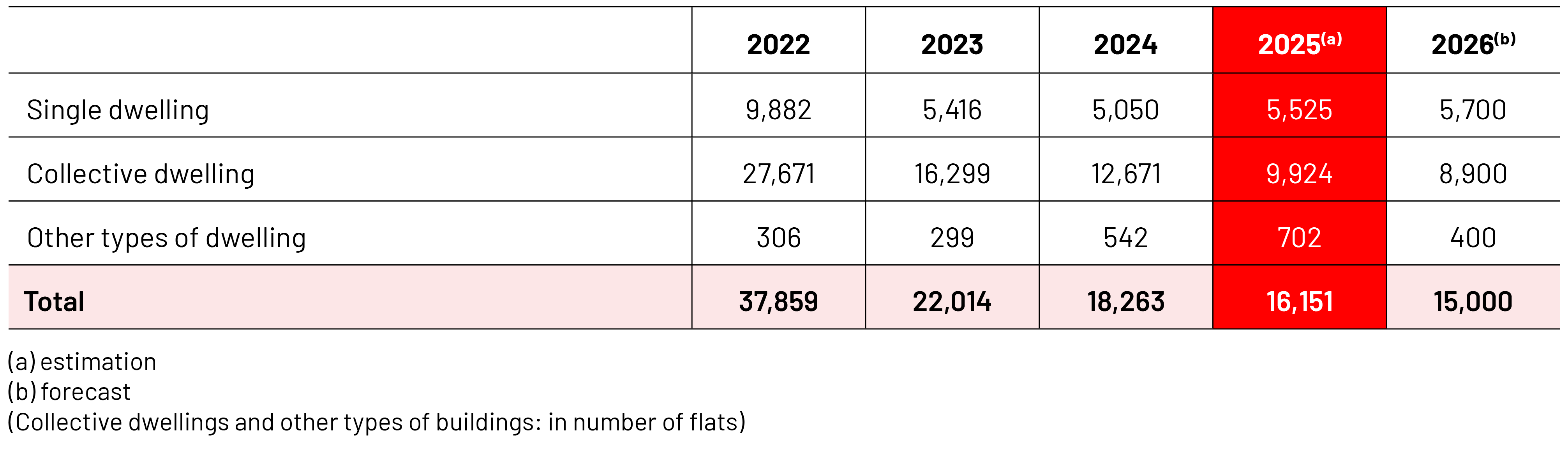

Residential construction declined last year for the fourth consecutive year, falling to only 16,900 housing units. Demand weakened across all segments. The volume of new housing production increased slightly due to a rise in the average apartment size and a late surge in publicly supported production. Housing prices and rents continued to decline. Supply remained abundant relative to the economic cycle in new homes, existing homes, and rental housing alike. Housing transactions and mortgage lending increased. No turnaround was seen in consumers’ intentions to purchase homes.

The housing market continues to be weighed down by high unemployment, weak consumer confidence, and tightening financial conditions. Growth in lending has shown signs of slowing both domestically and across the euro area. The decline in prices and rents continues to weaken economic profitability throughout the value chain, while construction and financing costs remain elevated at the same time

Non-residential construction

The decline in non-residential construction continued last year for the fourth consecutive year. The recovery of private investments toward growth stalled due to the trade policy disputes in the spring. The decline in new construction starts continued, falling to 19 million cubic meters — a level last seen 20 years ago. The decrease in the volume of new production accelerated to 10 percent compared with the previous year.

Some recovery was seen last year in industry and the real estate market. In the private sector, growth occurred in commercial and office construction as well as transport-related buildings, driven by data centers. In the public sector, growth was seen in healthcare and educational buildings.

GDP 2025

BILLION

POPULATION 2025

Total investment in construction in 2025

BILLION

Civil engineering

The business cycle in civil engineering was slightly weaker at the end of last year than previously expected. According to preliminary data, investments declined by about one percent over the full year, but returned to growth after the sharp contraction seen in the first quarter of last year. Based on the first surveys of this year, the decline in order books and new orders appears to be continuing. Contractors’ willingness to bid has increased, and spare capacity is available. However, according to business cycle surveys, expectations for the current year remain positive. Public investments in security of supply and in reducing the infrastructure maintenance backlog will continue. Private investments are being weighed down by global uncertainty.

Prices of construction materials

Construction costs increased by just under one percent last year compared with the previous year. The rise in material costs was moderate, but labor costs increased sharply as a result of wage increases. The cost of other inputs declined significantly.

Business registration and bankruptcy

The number of bankruptcies declined slightly from the record-high level of the previous year. However, the number of bankruptcies remains high due to weak corporate financial performance and the slow recovery of the construction sector. New business registrations remained below their longer-term average.

Construction Activity

Number of building permits in residential construction