Overall construction activity

In 2025, GDP growth reached 1.5% in the European Union and 1.4% in the euro area. For 2026, growth is expected to slow down to 1.1% in the EU and 0.9% in the euro area, while inflation is projected to increase again, reaching 3.1% in the EU and 3.0% in the euro area. This weaker macroeconomic outlook, combined with persistent cost pressures, tighter financing conditions and lower private investment appetite, continues to weigh on the construction sector.

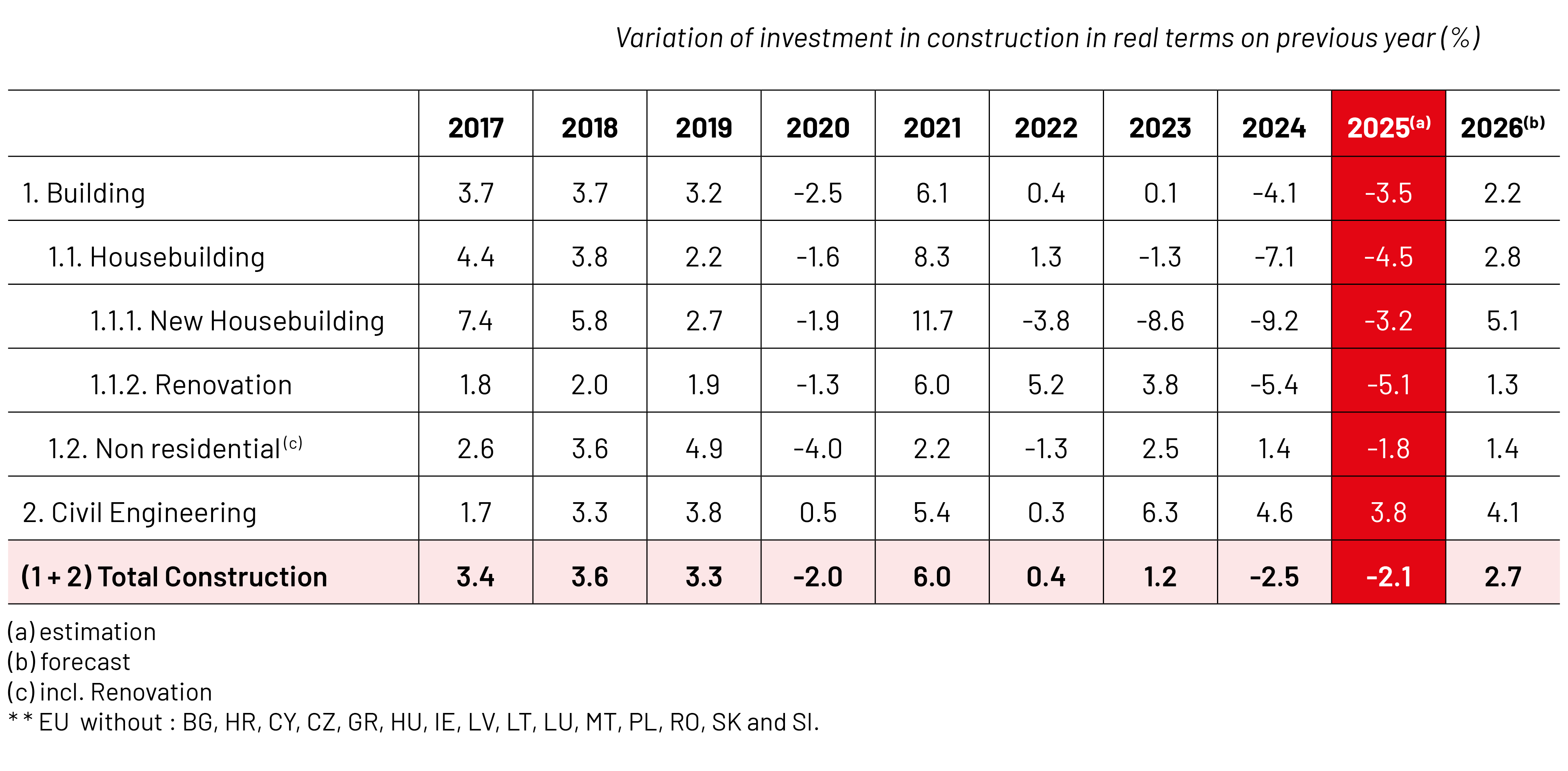

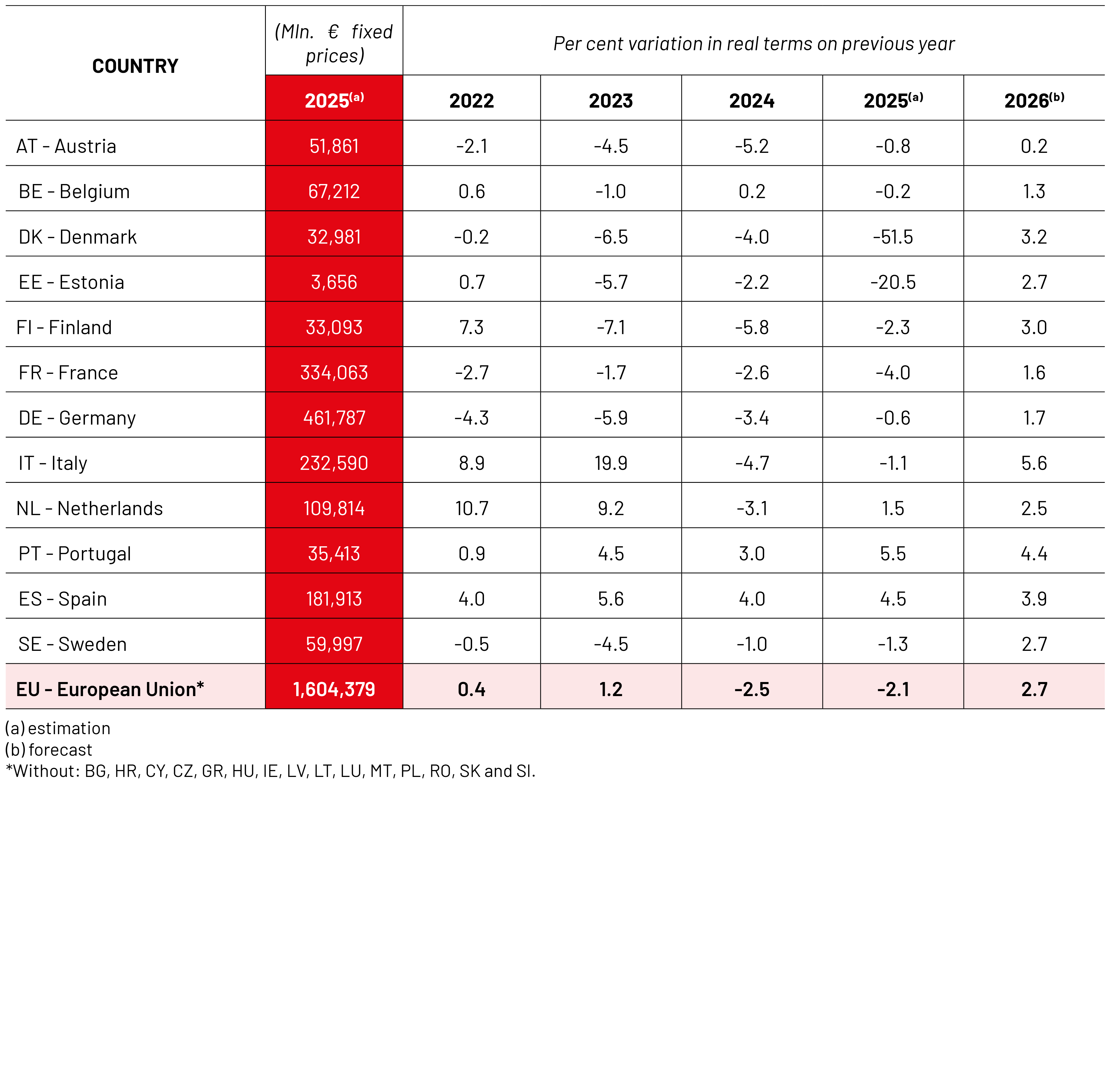

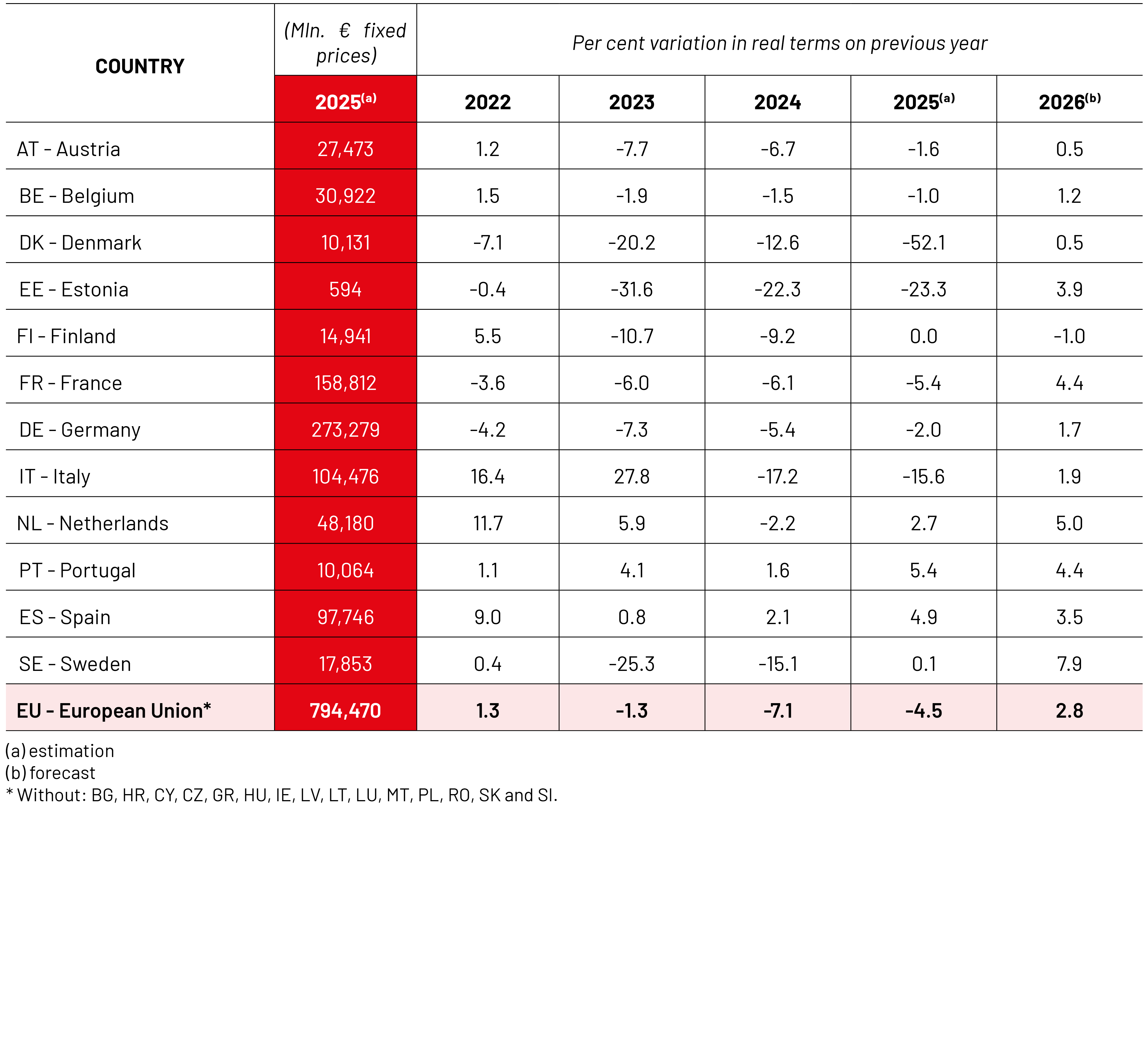

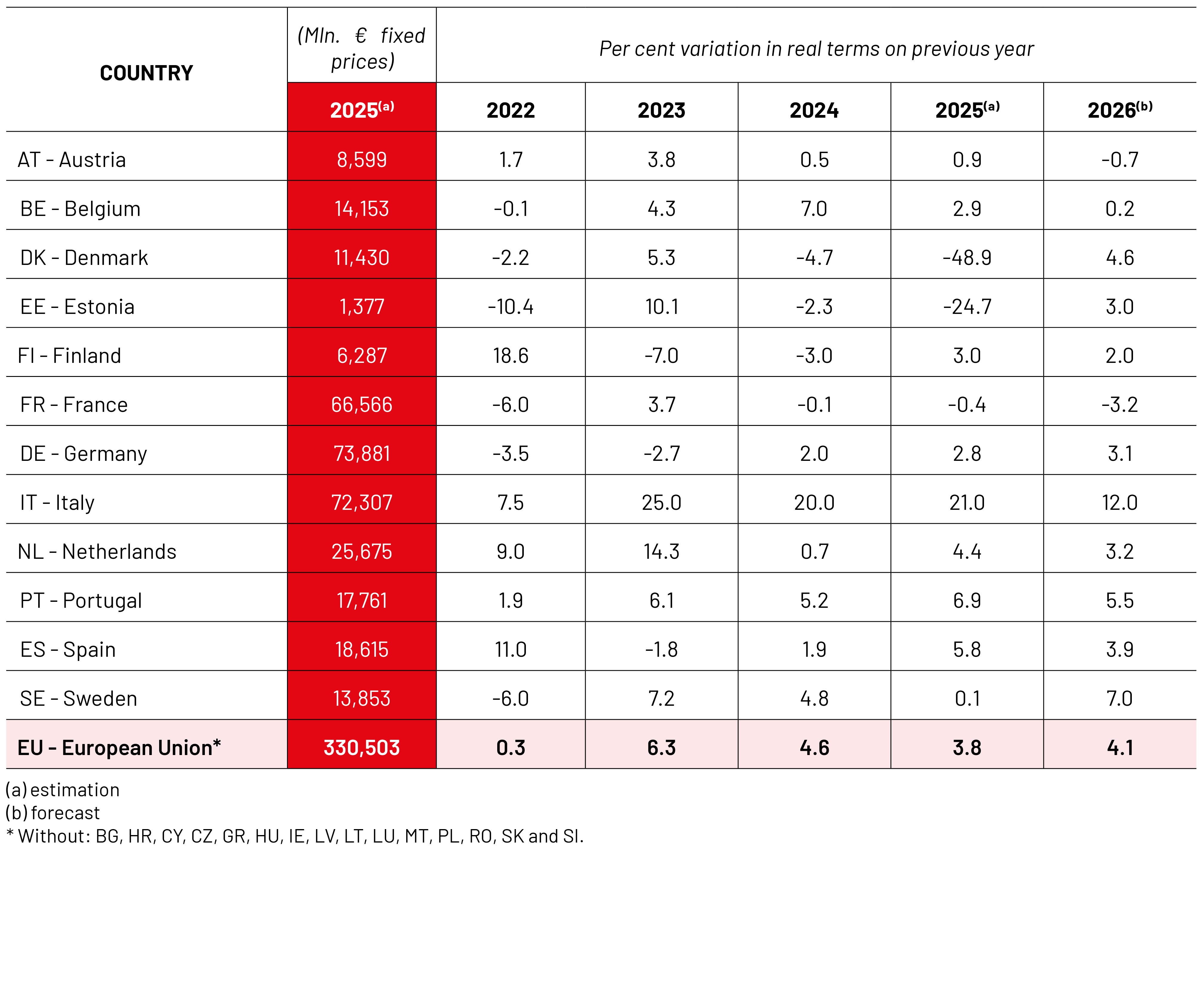

After two consecutive years of contraction, total investment in construction in the EU is expected to return to growth in 2026. In 2025, construction investment decreased by 2.1% in real terms, following a decline of 2.5% in 2024. This confirms that the sector remained under pressure throughout 2025, mainly due to the weakness of building construction and, more specifically, the continued adjustment in residential markets. Across the country reports, the same mechanisms recur: financing costs are still restraining private demand, while public investment and EU funds increasingly explain why some countries are outperforming the European average.

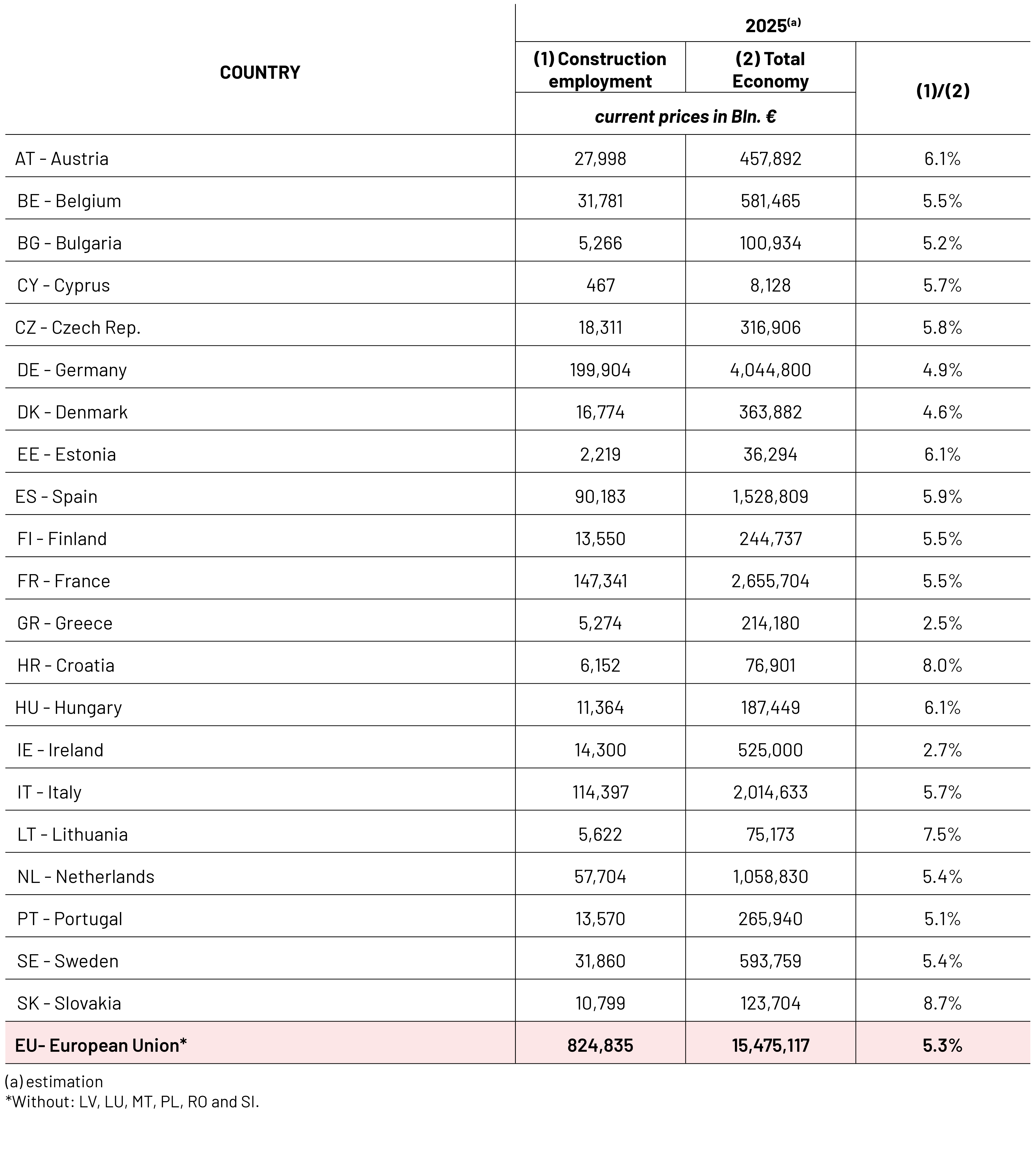

In current prices, investment in construction amounted to around EUR 1,353 billion in 2025, representing 8.1% of EU GDP. Construction gross value added reached EUR 824.8 billion in the EU sample, corresponding to 5.3% of the total economy. The construction industry also remains a major employer, accounting for around 6.5% of total employment and 31.1% of industrial employment, with more than 12 million workers.

Looking at individual countries, the picture remained mixed in 2025. The strongest increases in total construction investment were recorded in Portugal (+5.5%), Spain (+4.5%) and the Netherlands (+1.5%). Portugal and Spain benefited from stronger domestic demand and EU-funded public investment, while the Dutch recovery was helped by earlier residential permits and by investment in networks and water infrastructure. By contrast, several markets remained in decline, including France (-4.0%), Finland (-2.3%), Sweden (-1.3%), Italy (-1.1%) and Germany (-0.6%). In Germany, the weakness remains closely linked to residential affordability, as mortgage rates and residential construction prices are still far above pre-crisis levels. In France, the expected housing rebound is partly offset by a more difficult outlook for public works. Particularly sharp decreases were recorded in Estonia (-20.5%) and Denmark (-51.5%). The Danish figure should be read with caution, as the data show a significant break in the level of the series between 2024 and 2025.

The outlook for 2026 is more positive, with total construction investment expected to increase by 2.7%. This would mark the first year of recovery after the downturn observed in 2024 and 2025. However, the rebound is expected to be moderate and does not fully compensate for the losses recorded during the previous two years. In volume terms, total construction investment would remain below its 2023 level.

The recovery is expected to be led by Italy (+5.6%), Portugal (+4.4%) and Spain (+3.9%). Italy is a special case: the positive forecast is largely driven by the final acceleration of NRRP infrastructure projects, while the residential market remains weak after the reduction of housing tax incentives. Finland (+3.0%), Sweden (+2.7%) and the Netherlands (+2.5%) are also expected to return to positive growth. In the two largest construction markets, Germany (+1.7%) and France (+1.6%), the recovery is expected to remain subdued, suggesting that the main Western European markets are not yet entering a strong expansion phase.

At segment level, the expected improvement in 2026 is mainly due to a return to growth in building construction and the continued resilience of civil engineering. Building investment is forecast to grow by 2.2% after a decline of 3.5% in 2025, while civil engineering is expected to remain the strongest segment, with growth of 4.1%.

The figures for 2026 point to a moderate recovery in the European construction sector after two difficult years. Total construction investment is expected to grow by 2.7%, supported by a rebound in building activity and continued strength in civil engineering. Nevertheless, the recovery remains uneven across segments and countries. In practice, the divide within Europe is increasingly between countries where public investment, EU funds and infrastructure pipelines are already feeding through to activity, and countries where the recovery still depends on private developers restarting projects under tighter financial conditions.

New housebuilding is expected to return to growth, but this follows a deep downturn and does not yet indicate a full recovery of residential markets. Renovation remains below its potential, despite its strategic importance for climate policy. Non-residential construction is stabilising, while civil engineering continues to be the most reliable growth driver.

Overall, the European construction sector enters 2026 in a better position than in 2025, but still faces significant risks. Financing conditions, public investment capacity, energy and material costs, administrative delays and company solvency will remain decisive factors for the pace and durability of the recovery.

GDP 2025

BILLION

POPULATION 2025

Total investment in construction in 2025

BILLION

Housebuilding

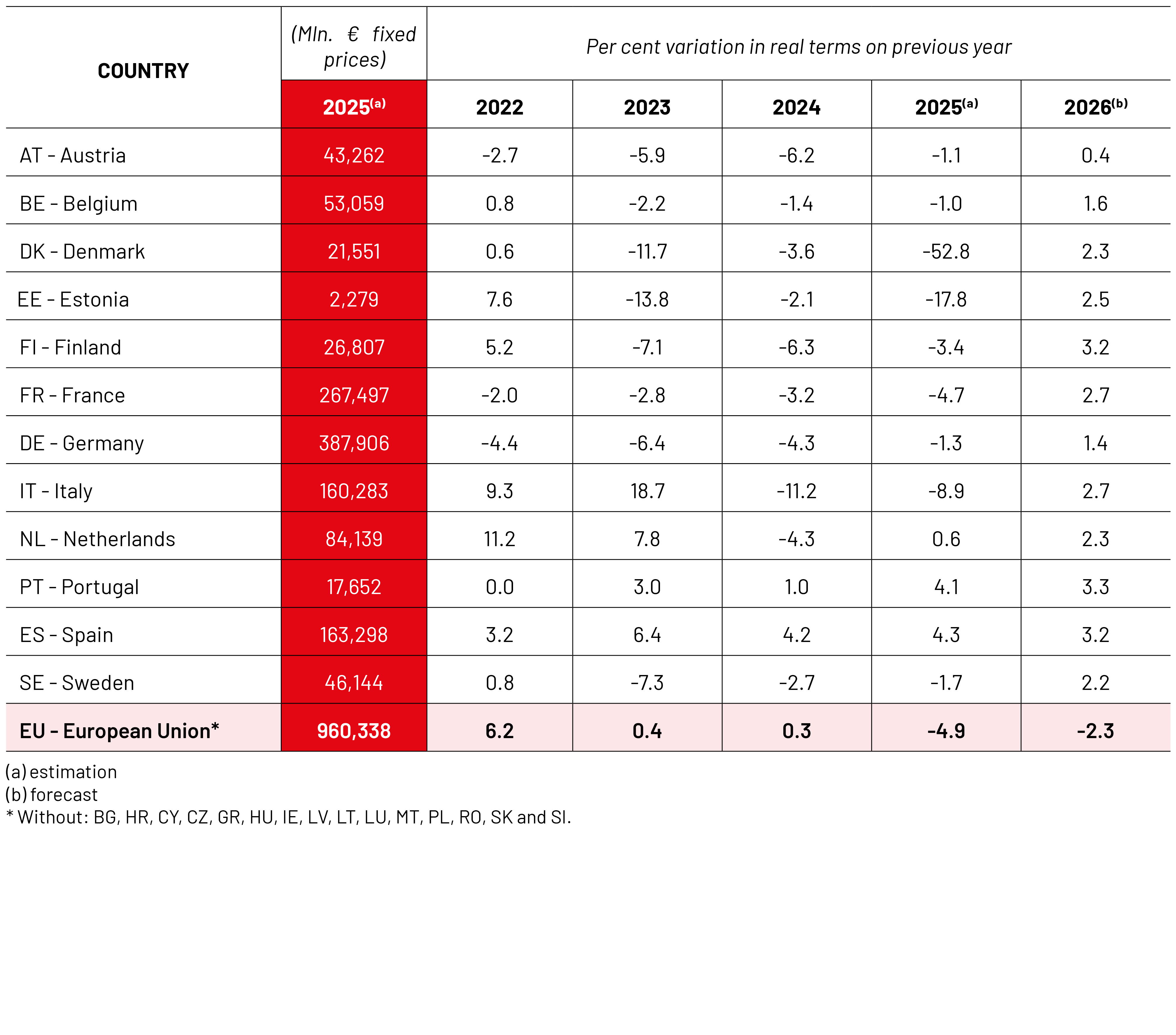

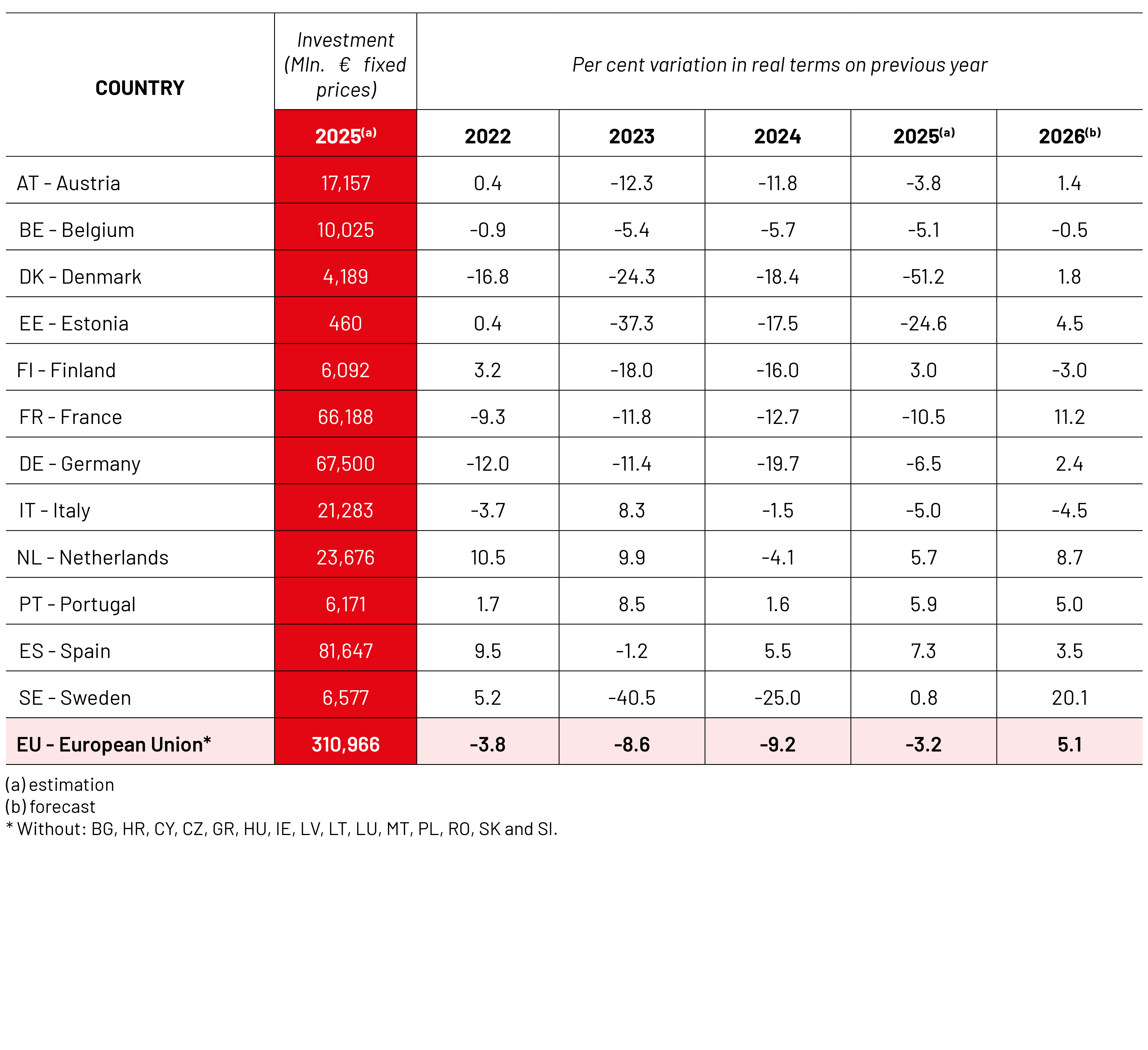

Housebuilding, including both new housebuilding and renovation, represents close to half of total construction investment. In 2025, this segment continued to be the main source of weakness for the construction sector, with investment declining by 4.5% after a sharper fall of 7.1% in 2024. The segment remains highly exposed to interest rates, household purchasing power, construction costs and the availability of housing finance.

New housebuilding represents around 19.8% of total construction investment. After a severe contraction of 9.2% in 2024, investment in new housebuilding decreased again in 2025, by 3.2%. This indicates that the downturn in the residential market continued, although at a slower pace than in the previous year. The weakest performances in 2025 were recorded in Denmark (-51.2%), Estonia (-24.6%), France (-10.5%), Germany (-6.5%) and Belgium (-5.1%). Italy also remained negative (-5.0%). In Germany and France, the weakness still reflects the same affordability equation: higher financing costs, high construction prices and a low number of viable projects. In Italy, the downturn is more policy-driven, as the withdrawal of generous housing tax incentives continues to affect the residential market. On the other hand, Spain (+7.3%), Portugal (+5.9%), the Netherlands (+5.7%) and Finland (+3.0%) recorded positive growth. In Spain and Portugal, the figures should be read against a background of persistent housing shortages, while in the Netherlands the pipeline of permits issued in previous years is supporting completions.

The outlook for 2026 is more encouraging. Investment in new housebuilding is expected to grow by 5.1%, making it one of the strongest contributors to the overall recovery. The sharpest increases are forecast in Sweden (+20.1%), France (+11.2%), the Netherlands (+8.7%) and Portugal (+5.0%). The Swedish rebound should also be read as a recovery from a very low base, supported by lower variable rates, improving housing prices, rising real incomes and easier credit conditions after the 2023-2024 housing crisis. However, this recovery should be interpreted carefully, as it comes after several years of strong decline in some markets. New housebuilding would therefore be entering a phase of partial rebound rather than a full return to pre-crisis levels.

For housebuilding as a whole, investment is expected to increase by 2.8% in 2026. Sweden (+7.9%), the Netherlands (+5.0%), Portugal (+4.4%) and France (+4.4%) are expected to record the strongest growth. Finland is the only country in the sample where housebuilding is expected to decline further in 2026 (-1.0%).

Overall, the residential segment appears to be stabilising, but the market remains fragile. The expected rebound in 2026 will depend on the evolution of financing conditions, housing demand, the speed of permitting procedures and the capacity of developers to restart postponed projects.

Rehabilitation/Maintenance

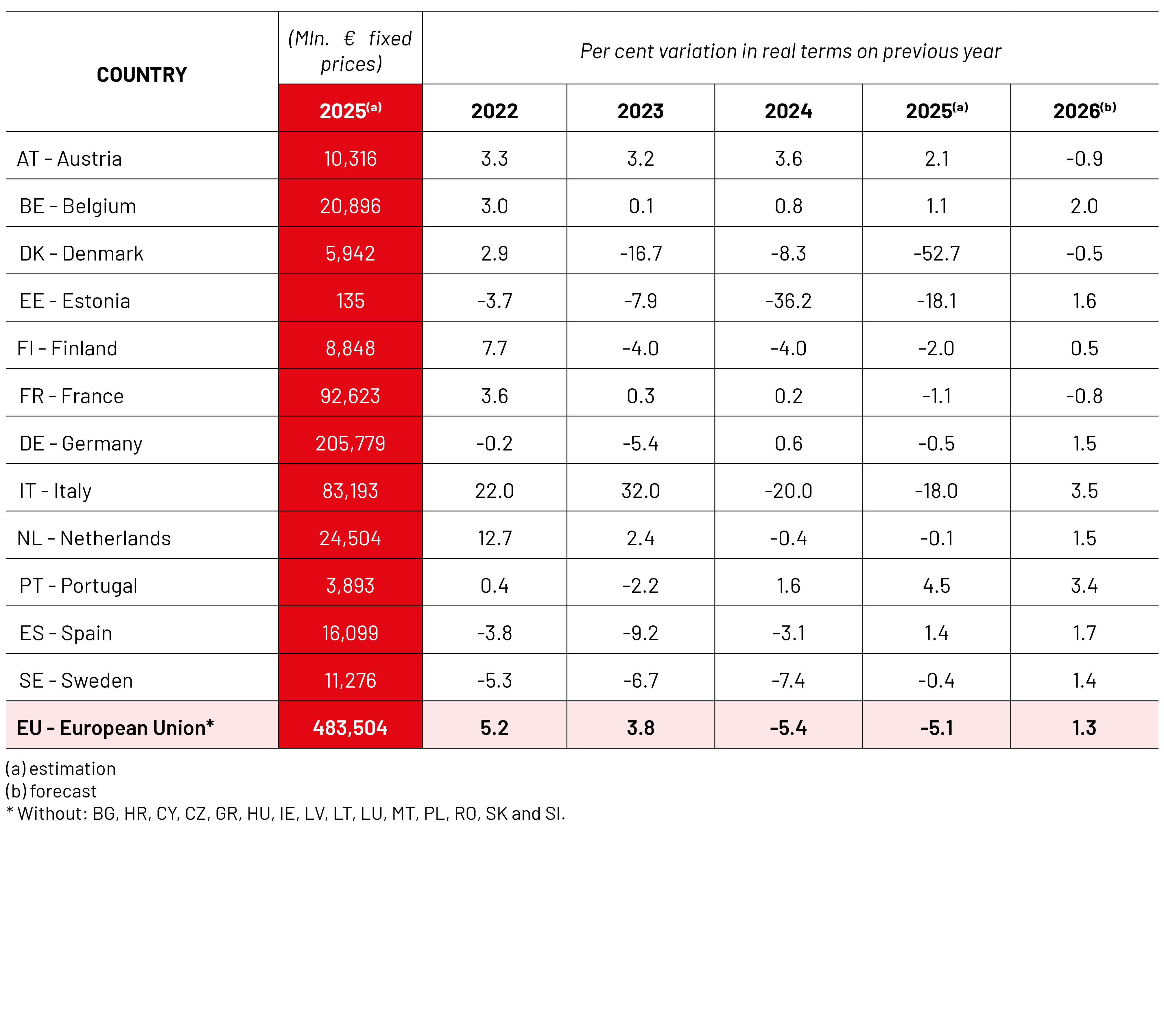

Investment in renovation represents around 29.6% of total construction investment. Traditionally, this segment has been less volatile than new construction and has often played a stabilising role during downturns. However, in 2025, renovation investment also contracted significantly, falling by 5.1% after a decline of 5.4% in 2024.

This underperformance is notable because renovation remains central to European and national climate policies, particularly in relation to energy efficiency, decarbonisation of the building stock and the reduction of household energy consumption. In the short term, however, the data suggest that renovation has not been able to fully offset the weakness of new housebuilding. Italy is the clearest illustration of how dependent this market can be on policy incentives: the phase-out of tax measures that previously supported residential renovation has turned a former growth driver into one of the main drags on the segment.

At country level, growth in renovation investment in 2025 was recorded in Portugal (+4.5%), Austria (+2.1%), Spain (+1.4%) and Belgium (+1.0%). By contrast, sharp declines were observed in Denmark (-52.7%), Estonia (-18.1%) and Italy (-18.0%). More moderate decreases were recorded in Finland (-2.0%), France (-1.1%) and Germany (-0.5%).

In 2026, renovation investment is expected to return to positive growth, but only moderately, with an increase of 1.3%. Italy (+3.5%), Portugal (+3.4%), Belgium (+2.0%) and Spain (+1.7%) are expected to show the strongest growth. France (-0.8%) and Austria (-0.9%) are forecast to remain slightly negative. In Spain, the Recovery Plan remains an important support for energy renovation, but implementation has been slower and less agile than expected; in France, budget timing and weaker housing transactions continue to weigh on the market.

The renovation segment therefore continues to offer important long-term potential for the construction sector, but the 2025 and 2026 figures show that policy ambition does not automatically translate into immediate market growth. Public support schemes, stable regulatory frameworks and access to finance will remain decisive for turning renovation into a stronger driver of activity.

Non-residential construction

Non-residential construction represents around 29.9% of total construction investment. After modest growth in 2024 (+1.4%), the segment contracted by 1.8% in 2025. This confirms that non-residential construction, although more resilient than the residential segment, was not immune to the broader slowdown in investment.

In 2025, the strongest growth was recorded in Italy (+8.1%), Spain (+3.3%) and Portugal (+2.4%). Germany recorded a slight increase (+0.6%), while Austria remained almost stable (-0.2%). Several countries registered declines, including Finland (-7.0%), France (-3.8%), Sweden (-2.8%) and the Netherlands (-2.2%). Estonia and Denmark recorded much sharper decreases. The Dutch case is particularly illustrative: retail and office demand remained weak, while nitrogen and phosphate constraints, grid congestion and a slower conversion pipeline continued to hold back parts of the market.

The outlook for 2026 points to a moderate recovery, with non-residential construction expected to grow by 1.4%. The strongest increases are forecast in Finland (+8.0%), Italy (+4.2%), Denmark (+4.0%) and Spain (+2.7%). Growth is expected to be more limited in France (+0.2%), Germany (+0.8%) and Sweden (+1.0%), while the Netherlands is expected to decline further (-1.5%). In Germany, data centres and defence-related public demand offer some support, but industrial investors remain cautious in a weak export environment.

Overall, non-residential construction appears to be stabilising rather than expanding strongly. Activity in this segment will continue to depend on business investment, public-sector projects, demand for industrial and logistics buildings, and the capacity of local authorities to finance social infrastructure such as schools, hospitals and public buildings.

Civil engineering

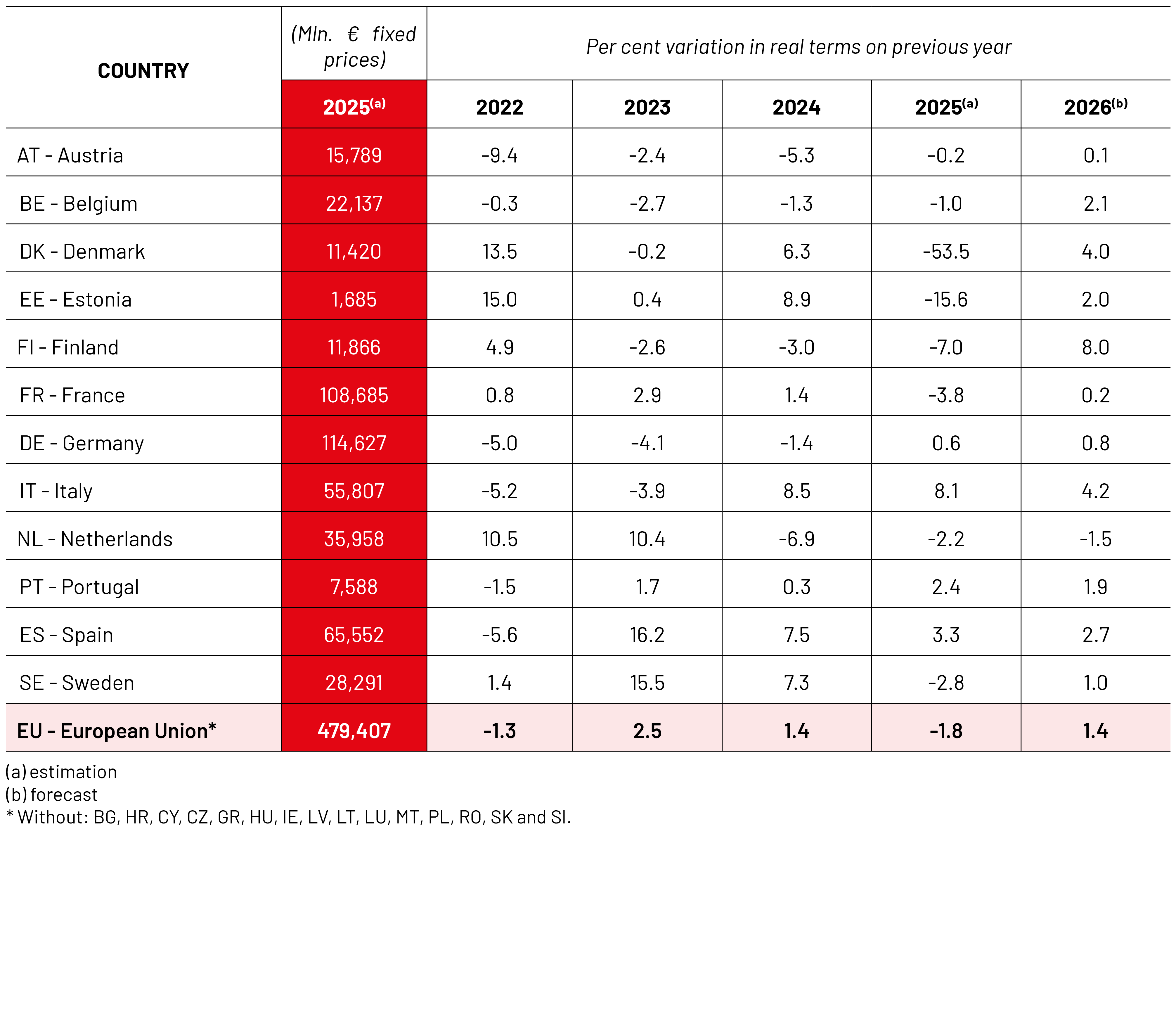

Civil engineering represents around 20.6% of total construction investment. It remained the strongest and most resilient segment in 2025, growing by 3.8% after an increase of 4.6% in 2024. In a context of weak building activity, civil engineering continued to play a stabilising role for the construction sector. This is also the segment where the difference between countries with an active public-investment pipeline and those facing budget constraints is most visible.

The performance of civil engineering is largely linked to public investment, infrastructure modernisation, transport projects, energy networks and investments connected to the green transition. The segment has also benefited from European and national funding programmes, although the timing of project implementation varies significantly between countries.

In 2025, the strongest growth in civil engineering was recorded in Italy (+21.0%), followed by Portugal (+6.9%), Spain (+5.8%), the Netherlands (+4.4%) and Finland (+3.0%). Italy is the clearest example of this pattern, with NRRP projects - particularly rail and local infrastructure - turning civil engineering into the main engine of the sector. Growth was more moderate in Belgium (+2.9%), Germany (+2.8%) and Austria (+0.9%). France recorded a slight decline (-0.4%), while Estonia and Denmark posted much sharper decreases.

The outlook for 2026 remains positive. Civil engineering investment is expected to grow by 4.1%, making it the strongest segment for the second consecutive year. The highest growth rates are forecast in Italy (+12.0%), Sweden (+7.0%), Portugal (+5.5%), Denmark (+4.6%) and Spain (+3.9%). In Denmark and the Netherlands, energy networks, water infrastructure and large transport projects help explain why civil engineering performs better than building activity. Germany (+3.1%), the Netherlands (+3.2%) and Finland (+2.0%) are also expected to grow. By contrast, civil engineering investment is forecast to decline in France (-3.2%) and Austria (-0.7%). In France, this expected decline reflects local budget cuts, the municipal election cycle and political uncertainty, which weigh more directly on public works than on private building activity.

Civil engineering is therefore expected to remain a key support for the European construction sector in 2026. However, its capacity to compensate for weakness in building construction remains limited by its smaller share in total investment. The medium-term outlook will depend on public budgets, the absorption of EU funds, procurement capacity and the ability of contractors to manage cost and labour constraints.