Overall construction activity

Italian GDP recorded a moderate increase of +0.5% year-on-year in 2025, confirming the slowdown phase that has been underway since 2023. Economic activity was affected by the negative contribution of external demand: the imposition of tariffs and the appreciation of the Euro against the US dollar weakened export dynamics (+1.2%), while imports increased by +3.6%. At the same time, household consumption (+0.9%) did not rebound in line with expectations, as households continued to postpone spending decisions due to uncertainty. Conversely, investment remained the most dynamic component (+3.5%), specifically supported by the acceleration associated with the final phase of works related to the National Recovery and Resilience Plan (NRRP).

Italy’s growth prospects for 2026 remain highly dependent on developments in the recent conflict in the Middle East. In particular, the closure of the Strait of Hormuz, through which significant volumes of gas and oil transit, is leading to a substantial increase in the cost of raw materials and key consumer commodities, with negative consequences for both businesses and households. According to the latest Government forecasts included in the Public Finance Document, Italian GDP is expected to grow modestly by +0.6% year-on-year in 2026. However, this outlook is heavily influenced by the evolution of the global geopolitical context, which has become exceptionally complex and characterised by tensions and conflicts of uncertain duration and magnitude.

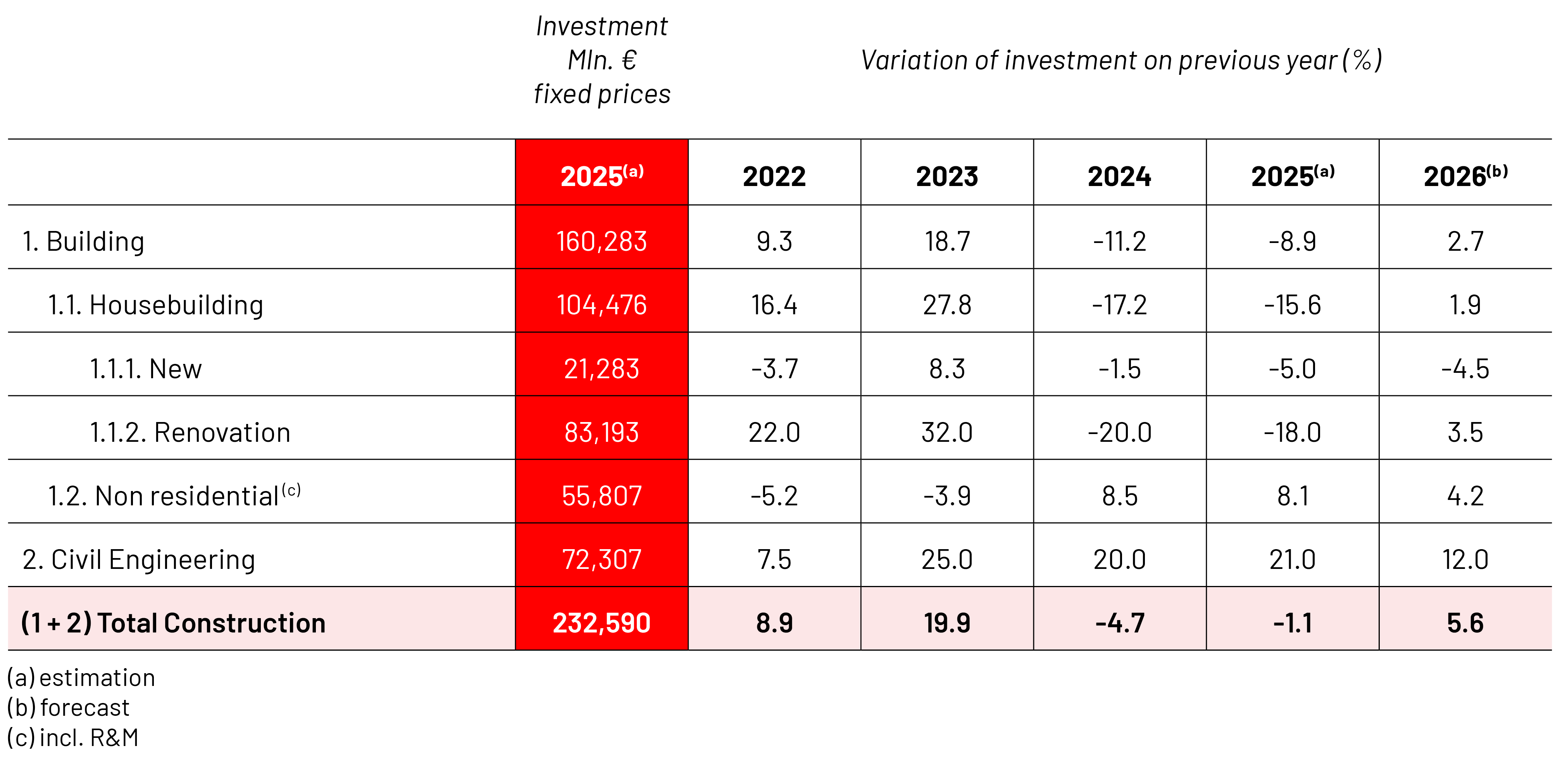

Against this backdrop, the construction sector – following a period of strong expansion that restored its role as a key driver of both economic growth and employment – recorded a moderate decline in production levels of -1.1% in 2025, according to the estimates of the National Association of Italian Constructors (ANCE). This figure represents a significant improvement compared to the estimate released one year earlier (-7%), due to a better-than-expected performance in civil engineering works, which accelerated sharply as a result of NRRP-related projects and largely offset the effects of the downsizing of tax incentives for the redevelopment of the housing stock. The new housing segment remains weak, while investment in housing renovation in the non-residential sector shows resilience.

ANCE’s forecast for 2026, released in January and therefore not accounting for the recent conflicts between the United States, Iran and Israel, points to a +5.6% increase in construction investment year-on-year. This result is strongly driven by civil engineering works, supported by the final acceleration of NRRP-related projects. A recovery in housing redevelopment is also expected, fostered by the extension of tax incentives and by growing household awareness of energy efficiency. Weakness persists in investment in new housing and new non-residential construction, mainly due to the decline in building permits, although early signs of recovery in authorised surface areas emerged in 2025.

Housebuilding

ANCE estimates that investment in housebuilding declined by -15.6% in real terms in 2025 compared to 2024.

This result is primarily driven by the progressive weakening of tax incentives for housing redevelopment, which has reduced the impact of one of the sector’s main growth drivers. In particular, the leading role of housing renovation has diminished significantly, after having accounted for approximately 40% of total investment.

More specifically, investment in new housing recorded a further real-terms decline of -5.0%. This trend is linked to the continued contraction in building permits, which have been decreasing steadily since 2022, with a reduction of -8.9% in 2023 and a further decline of -2.6% in authorised volumes in 2024.

The difficulties affecting new housebuilding are part of a broader and more complex “housing challenge”, which is not only Italian but also European in nature, and which led, at the end of 2025, to the preparation of a specific European Plan for housing affordability.

Returning to the national context, Italy has historically lacked a long-term strategy in housing policies, as evidenced both by the absence of targeted structural measures and by the lack of effective tools to monitor and analyse the evolution of housing needs. Over time, access to housing has become increasingly problematic not only for the most vulnerable groups, but also for wider segments of the population. In the absence of a forward-looking and integrated approach, the risk is that the housing crisis will further intensify, with significant implications not only for households, but also for national social cohesion and economic development. The Italian Government has recognised the importance of addressing this issue and has already increased available resources, also integrating European funding. As a result, a total allocation of approximately 8 billion Euro has been mobilised for the 2026–2032 period.

Turning to housing redevelopment, ANCE estimates a further decline of -18% in real terms in 2025 compared to the previous year. This trend is mainly due to the progressive reduction of tax incentives dedicated to such interventions, which in the past had played a crucial role in supporting the segment and, particularly during the protracted decade-long sectoral crisis, helped mitigate overall losses.

Looking ahead to 2026, ANCE forecasts a first recovery in housing redevelopment (+3.5%), supported by the extension of tax incentives and the growing attention of households to energy efficiency. Investment in new housing is expected to remain negative (-4.5%), mainly due to the decline in building permits, although early signs of recovery began to emerge in 2025.

Non-residential construction

In 2025, ANCE estimates that private investment in non-residential construction increased modestly by +0.5% year-on-year in real terms. This result reflects a combination of continued positive performance in extraordinary maintenance activity and a decline in new investments.

In particular, renovation and redevelopment activities are expected to grow further by +1%, following the already positive performance recorded in the previous year (+3.8%). Key segments – such as retail, hospitality and logistics – continue to provide a positive contribution, as they are effectively capturing ongoing market transformations and evolving demand patterns, demonstrating strong adaptability and resilience.

By contrast, new private non-residential developments are estimated to decline by -1.5% compared to 2024. This reflects the persistence of a negative trend in building permits (granted volumes) for non-residential construction, which has been underway since 2023.

Looking ahead to 2026, a moderate decline of -1.2% is expected year-on-year, reflecting a sharper contraction in new developments (-3.0%) and a stagnation in extraordinary maintenance activities (-0.8%).

GDP 2025

BILLION

POPULATION 2025

Total investment in construction in 2025

BILLION

Civil engineering

ANCE estimates that investment in civil engineering increased further by +21% in real terms in 2025. This result reinforces the positive trend observed in recent years, positioning civil engineering works as the new driver of growth for the construction sector, as well as for the Country’s infrastructure modernisation.

In this context, the NRRP continues to play a fundamental role. The latest data as of 31 December 2025 indicate that expenditure for the construction sector reached 37.6 billion Euro, excluding approximately 14 billion Euro of private-sector investment supported by the “Superbonus” measure. This spending is mainly concentrated on railway infrastructure and local-scale projects managed by local authorities.

ANCE’s outlook for 2026 envisions a further and significant increase in civil engineering investment, with a projected growth of +12% year-on-year, driven by the necessary acceleration in the final phase of NRRP-related interventions.

Construction Activity

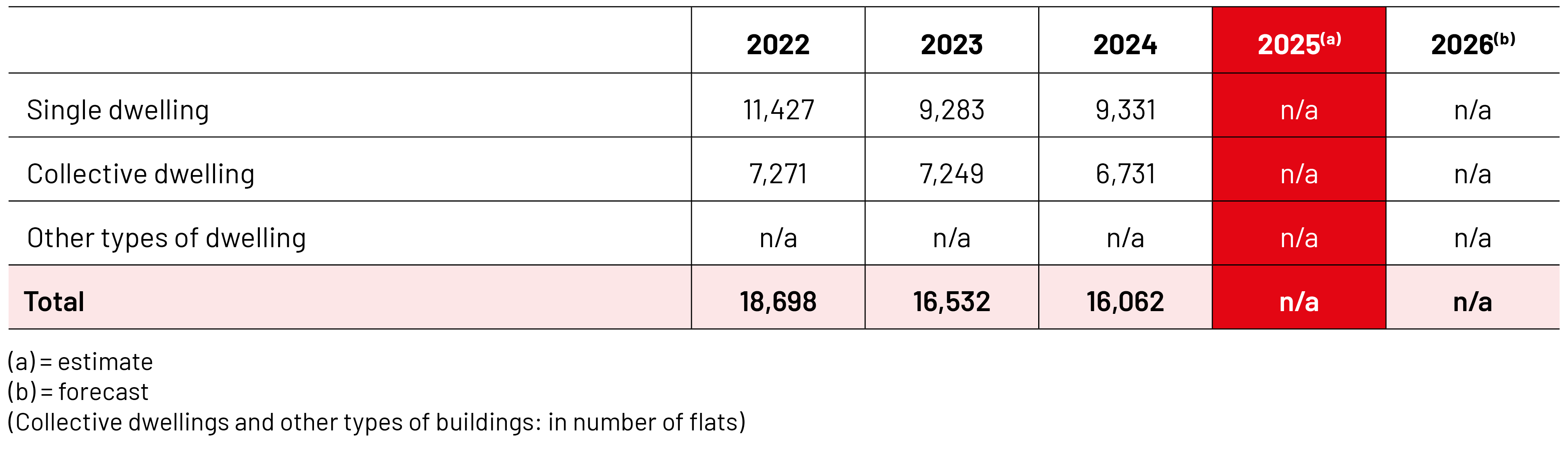

Number of building permits in residential construction