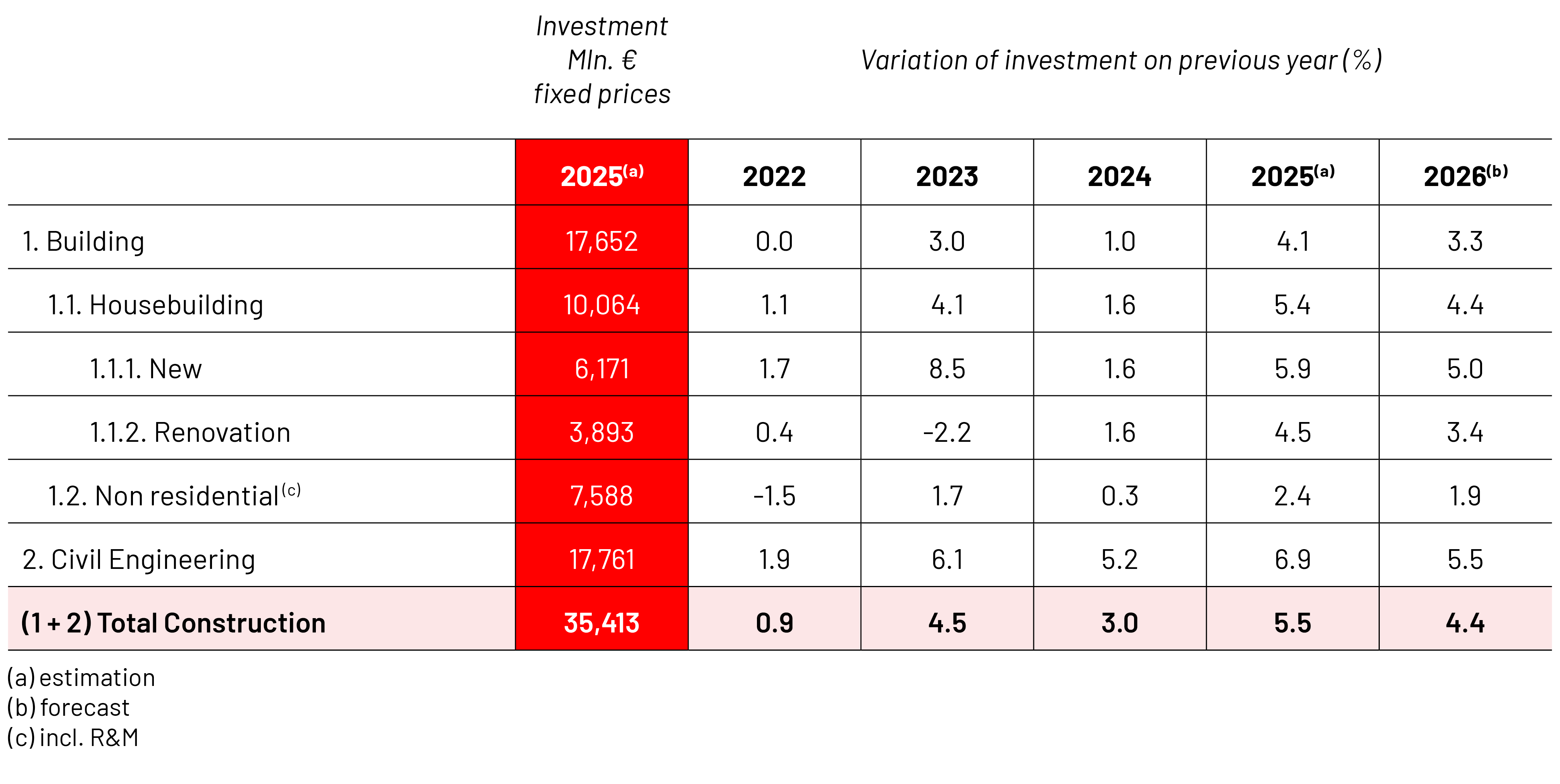

Overall construction activity

In 2025, the construction sector in Portugal maintained a robust growth trajectory, with Gross Value of Production increasing by approximately 4.1%, against a backdrop of national GDP growth of 1.9%. This economic performance was primarily supported by domestic demand, particularly private consumption, amid moderating inflation (2.2%) and the recovery of household disposable income. Investment also played a decisive role, notably Gross Fixed Capital Formation (GFCF) in construction, which grew by approximately 5.5%, driven by the implementation of European funds under the Recovery and Resilience Plan (RRP) and Portugal 2030.

Available data highlight the strengthening of investment dynamics in the sector, with GFCF in construction recording significant growth in 2025, continuing the upward trend observed in previous years and reflecting the impact of intensified EU fund execution and the gradual recovery of activity. In parallel, employment in the sector continued to expand, approaching 373,000 workers in 2025, reflecting the labor-intensive nature of the sector.

Despite this positive framework, significant structural constraints remain, namely the shortage of skilled labor, rising production costs, and lengthy licensing procedures—factors that continue to limit the sector’s capacity to respond effectively to market needs.

For 2026, the outlook points to the continuation of a growth trajectory for the construction sector, with an estimated expansion of around 4% in real terms. This performance is expected to remain supported by public investment and the execution of European funds, albeit with signs of moderation compared to the pace observed in 2025.

Investment in construction is projected to reach approximately €39.2 billion, reflecting the continuity of the investment cycle, although risks remain associated with the temporary nature of these stimuli. In this context, key challenges persist, particularly with regard to labor availability, administrative efficiency, and regulatory burdens, as well as the need to strengthen the sector’s productive capacity.

Residential construction

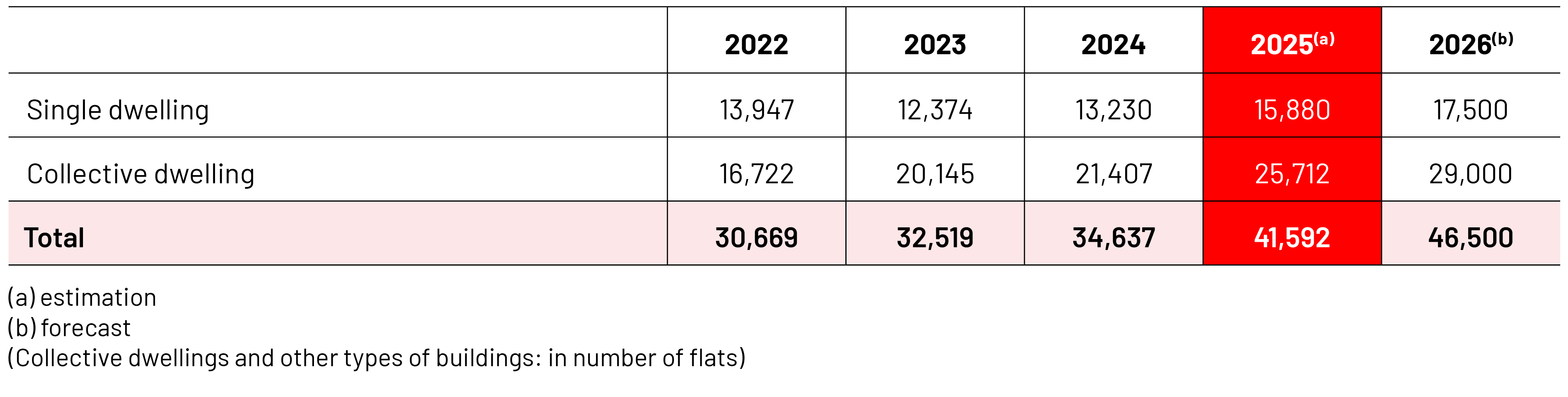

The housing segment performed particularly strongly in 2025, with an estimated 4.0% growth in production. This trend was accompanied by a significant increase in licensing activity, with the number of dwellings in new construction projects reaching approximately 41,591 units, reflecting a substantial increase of 20.1% compared to 2024.

In the first nine months of 2025, approximately 126,728 dwellings were transacted, corresponding to a year-on-year increase of 14.1%, driven particularly by existing housing (+15.2%). In value terms, transactions reached approximately €30.4 billion, reflecting growth of 28.4% and indicating a significant rise in investment in the residential sector.

The House Price Index recorded year-on-year increases in the range of 17% to 18% throughout 2025, reaching 17.7% in the third quarter, particularly in existing dwellings (+19.1%). This set of indicators confirms the persistence of a structural imbalance between supply and demand, as the production of new housing remains insufficient to meet market needs, thereby sustaining pressure on prices and affordability.

Non-residential construction

In 2025, the non-residential buildings segment recorded more moderate growth, estimated at approximately 1.0%. This evolution reflects a context of greater caution in private investment, shaped by interest rate levels and broader economic uncertainty. Licensing indicators corroborate this trend, showing a significant contraction in approved floor area for this type of building, suggesting a slower recovery of this segment compared to others.

GDP 2025

BILLION

POPULATION 2025

Total investment in construction in 2025

BILLION

Civil engineering

Civil engineering was the main driver of growth in the sector in 2025, with an estimated expansion of 5.5%, supported by strong public investment dynamics. In the public works market, indicators point to particularly high levels of activity. In 2024, the amount of tendered public works reached approximately €8.4 billion, reflecting a 39% increase compared to the previous year, while the value of contracts signed amounted to approximately €4.9 billion, corresponding to 32% growth. This momentum was maintained in 2025, driven by the acceleration of projects financed through European funds, with particular emphasis on the RRP.

Construction Activity

Number of building permits in residential construction